Money Market Update

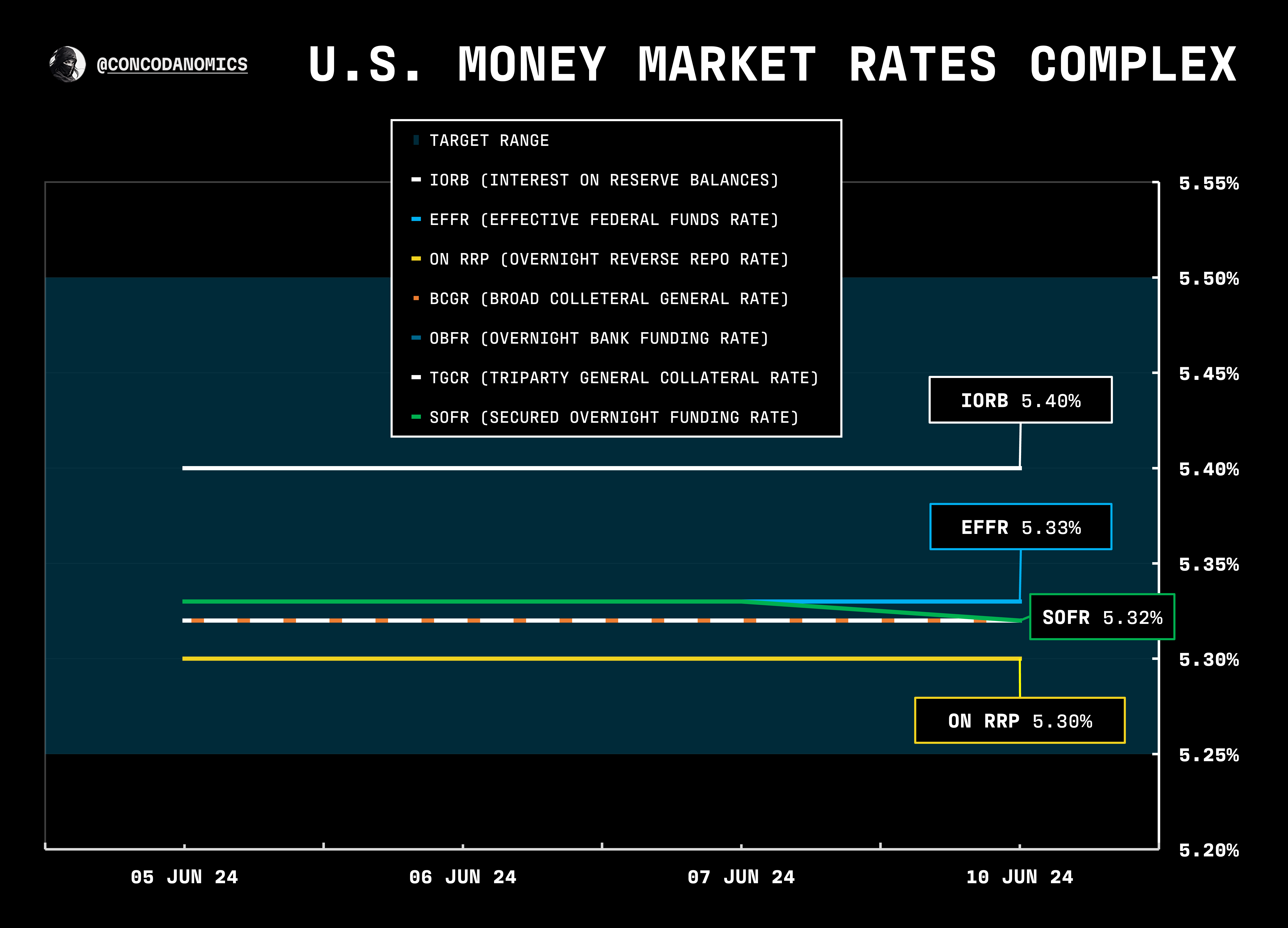

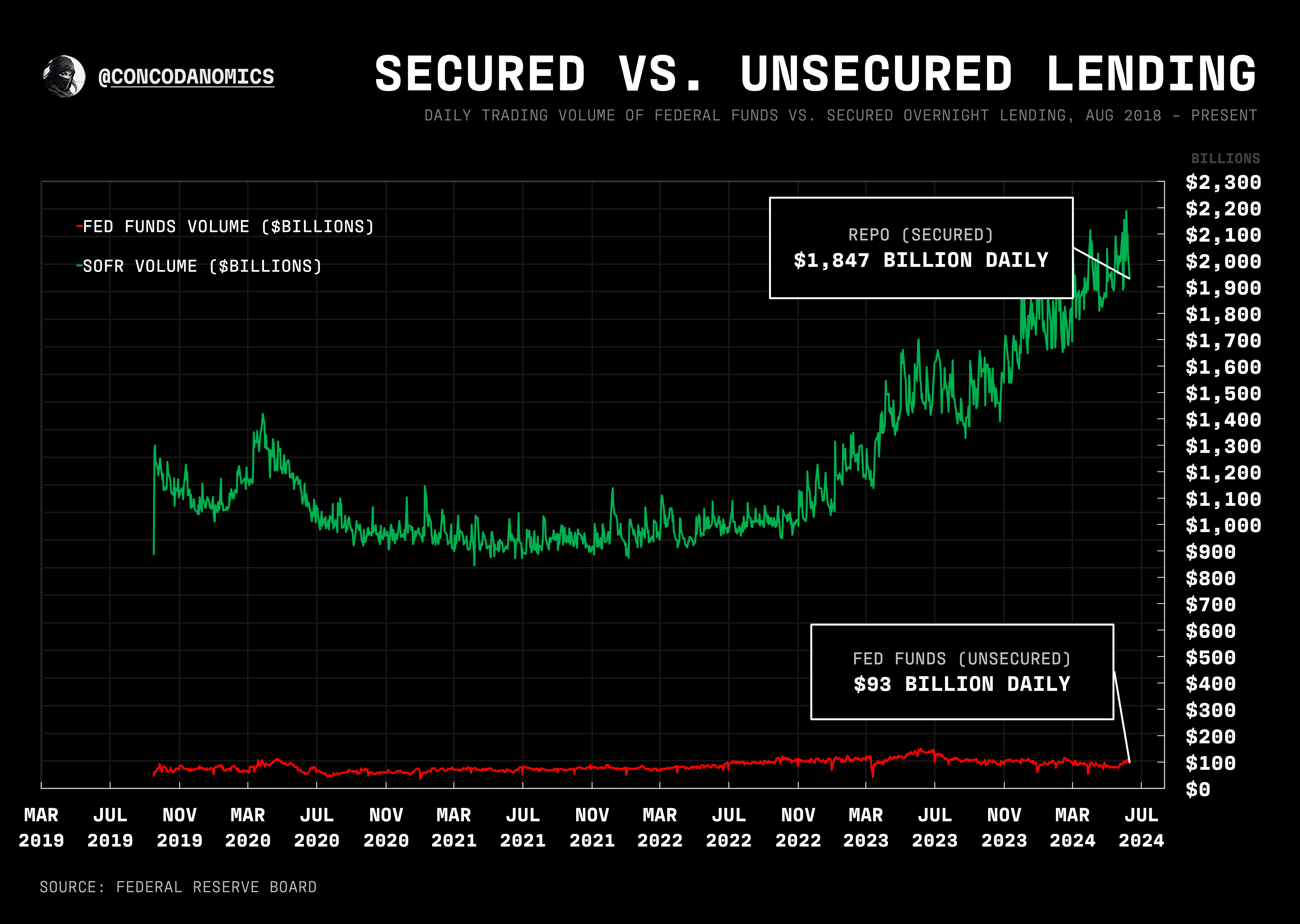

money market liquidity remains ample, with repo (SOFR) volumes approaching new heights alongside the Fed's foreign repo pool. bank reserves, meanwhile, remain elevated with a reduced QT

In case you missed it — or you’ve just joined us — part three of our Demystifying the Repo Market series went live…

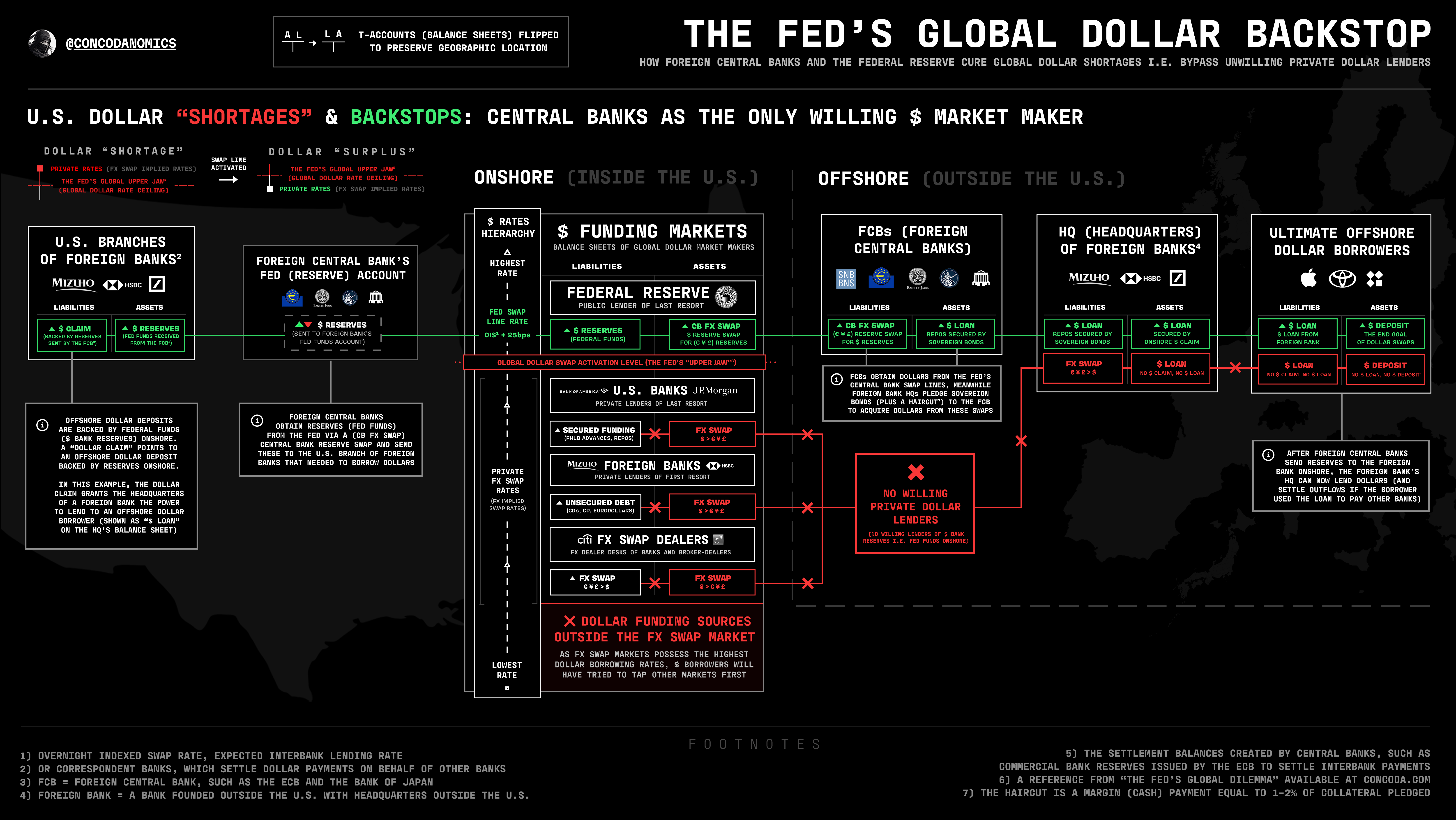

We hope you enjoyed the intricacies of the repo market, but now we’re taking a breather to explore other regions of the financial system. First up, the Fed’s new — and existing — “defense mechanisms.” A small taster below…

Now, onto the money market brief…

If you act on anything provided in this newsletter, you agree to the terms in this disclaimer. Everything in this newsletter is for educational and entertainment purposes only and NOT investment advice. Nothing in this newsletter is an offer to sell or to buy any security. The author is not responsible for any financial loss you may incur by acting on any information provided in this newsletter. Before making any investment decisions, talk to a financial advisor.

EFFR, OBFR, SOFR, TGCR, and BGCR are subject to the Terms of Use posted at newyorkfed.org. The New York Fed is not responsible for publication of tri-party data from the Bank of New York Mellon (BNYM) or GCF Repo/Delivery-versus-Payment (DVP) repo data via DTCC Solutions LLC (“Solutions”), an affiliate of The Depository Trust & Clearing Corporation, & OFR, does not sanction or endorse any particular republication, and has no liability for your use.

Hi Conks, I have a question in relation to the Foreign Repo. Is this actually QE like scenario, where the FED is just lending bills to other CBs to have dollar liquidity and if the actual Foreign RRP is increasing why the dollar doesn't have weakness?

After the BTFP execution, the volume of US Treasuries in the repo market plummeted.

Do you have any comments on this, as it seems that US Treasuries held in the BTFP should return to the market until next March?

I'd really like to hear what conks has to say.