Plumbing Feed: Swaps & Interventions

a roundup of posts from the Conks feed in article form

Welcome to a new type of Conks article: Plumbing Feed. First, it’s not obvious to new readers or those without the Substack app that we’re publishing additional thoughts via the chat (a.k.a Conks Feed). Second, some readers have also requested that the feed, not published on the main site due to post size, be published as articles. Thus, from now on, the Conks Feed will be reshared (not replaced) as a roundup in the following article format — and don’t worry: this format won't replace Plumbing Notes. To read chat posts as soon as they are published, join the feed here.

All the best, C.

APRIL 22, 2026: LIQUIDITY AT THE (ULTRA) SHORT END

Peace at the ultra-short-end of the curve, at least until the Fed attempts an unsavory shrinkage of its balance sheet, remains intact. All plumbing gauges, from the SOFR-FF basis to swap spreads, indicate that frictions are minimal and liquidity is flowing, a dynamic that has spread to the rest of the UST (U.S. Treasury) curve (>1y).

In geopolitics, it takes two to TACO to maintain stability. in plumbing, it takes two powerful forces of the sovereign, buybacks and RMOs (reserve management operations/purchases), to aid debt market functioning amid large auction tails & outright selling. Cash management buybacks (CMBs), where the Treasury uses (TGA) cash to buy back previously issued bills, have reduced unwanted supply, while RMOs, where the Fed prints reserves to buy bills from primary dealers, reduce the need for dealers to warehouse (i.e., hold) more supply on their books. Buybacks & RMOs have been offsetting the cost of warehousing USTs, especially further out on the curve, where greater levels of duration risk linger. Since dealers are looking to earn spread, not speculate on direction, dealers use repos (and other derivatives) to hedge against the duration risk of holding USTs outright. This applies upward pressure to overnight (o/n) rates (and general money market rates), one of the only forces working against the Fed maintaining SOFR in their desired sweet spot — just below IORB.

As Conks has noted, dealers can’t clear their inventories as easily as they used to pre-COVID, due to (among other things) record high deficits and foreign investors & carry traders (ex-some parts of Europe) earning negative carry for holding FX-hedged USTs. This Great Balance Sheet Congestion continues to boost primary dealer holdings, especially at the belly (>2y <10y), to all-time highs. Overall, primary dealers are harboring a record net long UST position of over $500 billion. Balance sheets are jam-packed.

Nevertheless, market liquidity remains resilient, aided by private-sector innovations (such as an ever-increasing shadow cash market - see our “The Shadow Cash Market” Series). The U.S. empire, of course, is likewise full of alchemy. On top of incoming deregulation, the Fed has bought ~$200b via RMPs while Bessent’s Treasury has vacuumed the same amount of short-end supply via CMBs, not forgetting its other type of buyback (i.e., liquidity buybacks) targeting most of the curve.

Demand and supply play a key role in determining moves in ultra-short-end rates (<1y), such as o/n GC, but play a less important role in determining the direction of rates at the UST short-end (>1y). With the latter, imbalances merely exacerbate rate moves. The sovereign, however, is dampening volatility by the most in history. Front-end rates markets are more resilient... but at the cost of opportunity.

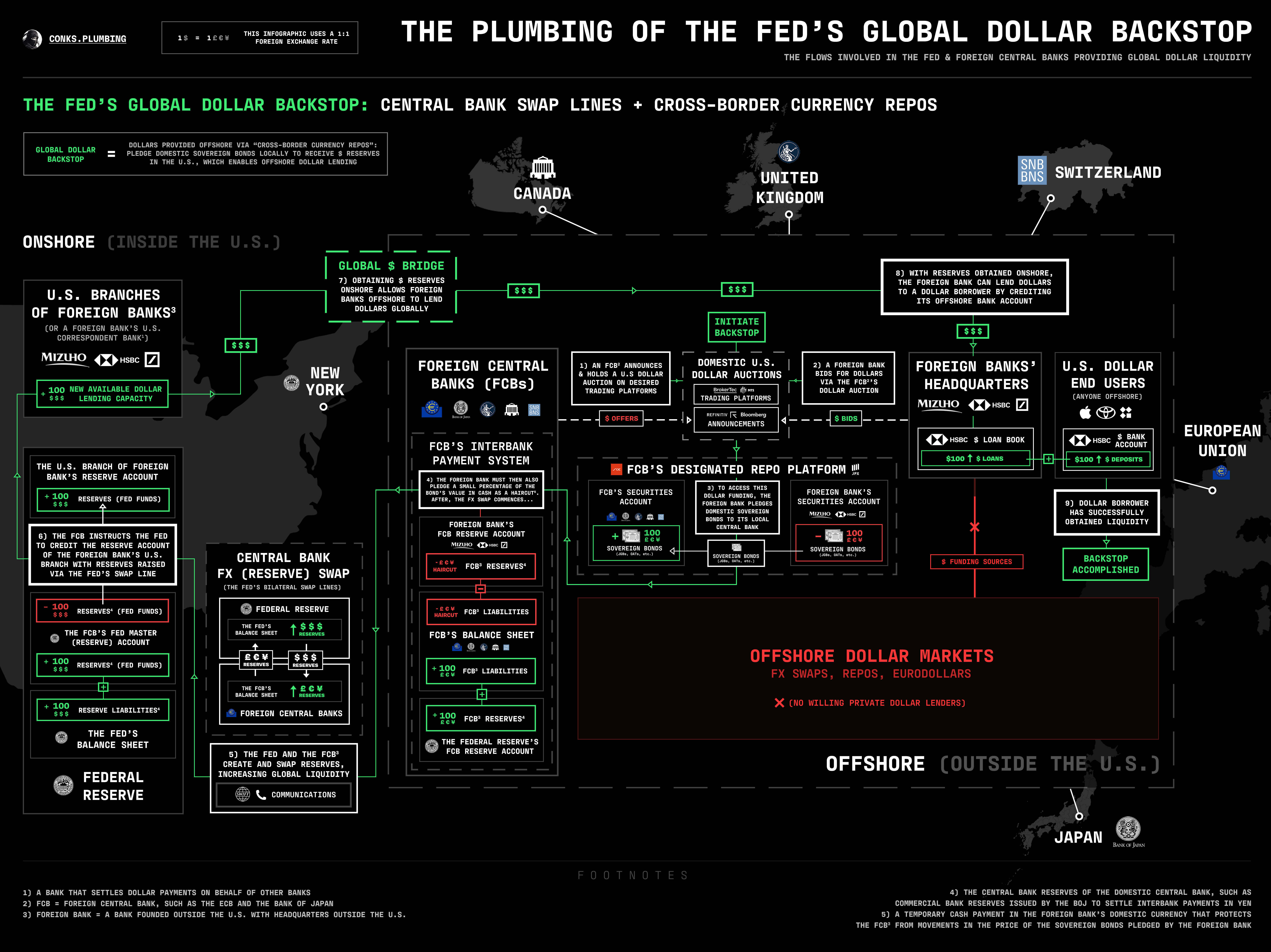

APRIL 23, 2026: WAR & DOLLAR SWAP LINES

In a testimony yesterday, Bessent mentioned that the UAE, other GCC states, and some Asian states requested $ swap lines to prevent potential firesales of USTs (U.S Treasuries). This is puzzling, considering all these nations have access to the Fed’s FIMA repo facility (pledge USTs and receive dollars in return, minus a 1-5% haircut depending on maturity), available to “public banks” like foreign central banks and finance ministries, where they don’t have to sell their holdings and can tap dollars at a cheaper (overnight) rate than receiving swap line liquidity.

Given the semi-relaxed state of global $ dollar funding markets and the fact that GCC states have more access to dollars via their SWFs (sovereign wealth funds) than available in the Treasury’s stabilization fund, the actual need for (and market impact of a) swap line to Asia would be minimal, and why use it when you have cheaper alternatives to tap dollars?

All in all, a nothingburger (but a great reason to post a Conks infographic).

APRIL 27, 2026: NOTHING EVER HAPPENS (REDUX)

The two-week pause has morphed into something else entirely, but the Peak-TACO thesis of resilient equities and hesitant rates has nonetheless transpired. Iran is still deploying “War & Plumbing” tactics, such as uncertainty via mines, provoking a delayed opening of the Strait that shall not be named. Regardless, aside from short-term rates not repricing, markets have moved back to “nothing ever happens.”

As Warsh is starting to recapture the headlines following his eclectic confirmation hearing, plus Tillis dropping his boycott, existing catalysts should begin to have a more dominant impact on pricing in some markets. It’s the beginning of the end of smooth sailing for ultra-short-term rates desks, as the June ‘27 deadline for a centrally cleared Treasury market grows nearer. Participants finally start, from year-end, to exodus uncleared repo markets en masse (and potentially applying upward pressure to SOFR), alongside an attempt to reduce the Fed’s balance sheet as early as December. Year-end SOFR-FF (Dec’26), despite these impending pressures, is only hovering around a 4-5bps basis (i.e. the gap between SOFR and FF), and mispricings likely expand into next year (‘27).

Before Warsh, however, no official in the Old Guard will be trying to stoke volatility. As usual, with the comfort of potential rate cuts at the first sign of economic weakness, the brief pre-Warsh period will incur minimal drag on risk assets. meanwhile, immediate term SOFR-FF (SERFF) longs must take a — well-deserved — breather. short-end cross-currency (XCCY) bases and swap spreads should “rally” further, i.e. three-month XCCY basis tightening (less negative) and 2-year swap spreads widening (also less negative), as minimal tax day volatility proved funding market liquidity and resiliency has moved way into ample territory.

Likewise, no one is trying to spur volatility at the long end of the curve. Bessent is busy playing macro with even more (this time, questionable) strategies to dampen long-end sales from Asia. Even so, investors are also remembering what Warsh could unleash. The fear of the new Fed Chair raising “term premium”, or whatever investors like to call increased risk premium, will help fuel cuts, but more likely spur an even greater UST steepener.

READ AS SOON AS THEY'RE PUBLISHED:

If you act on anything provided in this newsletter, you agree to the terms in this disclaimer. Everything in this newsletter is for educational and entertainment purposes only and NOT investment advice. Nothing in this newsletter is an offer to sell or to buy any security. The author is not responsible for any financial loss you may incur by acting on any information provided in this newsletter. Before making any investment decisions, talk to a financial advisor.

EFFR, OBFR, SOFR, TGCR, and BGCR are subject to the Terms of Use posted at newyorkfed.org. The New York Fed is not responsible for publication of tri-party data from the Bank of New York Mellon (BNYM) or GCF Repo/Delivery-versus-Payment (DVP) repo data via DTCC Solutions LLC (“Solutions”), an affiliate of The Depository Trust & Clearing Corporation, & OFR, does not sanction or endorse any particular republication, and has no liability for your use.