The Fed's New Rescue Mechanism

the central bank's emergency facility is about to evolve

After a year of neutralizing losses on banks’ underwater assets, the Federal Reserve’s BTFP (Bank Term Funding Program) is about to expire. A facility once used to quash financial panic and stimulate markets has been abused by the very banks it aimed to safeguard. Subsequently, the U.S. central bank is not only about to commence an “emergency phaseout” but assemble a new version of its primary rescue mechanism.

In March 2023, the remnants of COVID-19’s speculative boom came back to haunt the banks and monetary leaders that enabled it. The failure of Fed officials and Silicon Valley Bank (SVB) executives to address the hazards of handling a vast amount of flighty deposits ended in a string of bank failures. After SVB declared an emergency restructuring on March 8th, its heavily concentrated VC investor base engaged in a coordinated exodus, pulling billions of dollars in uninsured bank deposits from the Silicon Valley giant. Following the spread of rumors on and off social media the next day, another $100 billion in deposits (and thus reserves) was set to flee SVB’s balance sheet. Since obtaining more reserves to process further customer outflows required selling bonds heavily devalued by the Fed’s rate hikes, SVB’s equity cushion was set to be wiped out. Realizing they were toast, SVB executives contacted regulators, who promptly shuttered the bank’s doors on March 10th. Still, news of SVB’s collapse paired with Silvergate Bank’s earlier demise initiated a run on the regional banking system. By Friday’s market close, a mammoth Fed intervention was looming.

Upon resolving numerous failed banks and broadcasting further potential actions to calm the public, monetary leaders made their most assertive move to prevent financial turmoil from spreading. On March 12th, just before markets opened following a nervy weekend, the Fed announced the opening of its largest confidence booster: the Bank Term Funding Program, or BTFP for short. By enabling banks and other depository institutions to borrow cash (in the form of reserves) equaling the full (par) value of their securities — not the market value exposed to losses from rising interest rates, the Fed effectively bailed out banks’ interest rate (duration) risk.

Although this only applied to banks’ asset portfolios, the U.S. central bank indirectly signaled to market participants that it was willing to neutralize any amount of duration risk to maintain stability. Minus a tiny blip involving the long-awaited demise of investment banking giant, Credit Suisse, the Fed’s measures reignited sentiment, sparking a durable rally in risk assets. Quantitative Teasing™ had been unleashed.

As it happened, market participants correctly assessed the strength of the Fed’s interventions. Only a few poorly managed banks collapsed, while every other bank facing a squeeze turned to the BTFP for assistance. Increasing volumes at the Fed’s facility stoked fears that the banking turmoil had yet to conclude. But a few months later, the rise in BTFP loans outstanding began to slow, peaking at around $107 billion. As economic growth remained resilient and inflation rose at a slower pace, risk assets kept advancing, until increased issuance of longer-dated sovereign debt in Q3 provoked disruption in financial markets. The Treasury, however, soon performed a 180 and eased coupon issuance, marking the start of one of the sharpest equity rallies ever witnessed. By December 2023, the Fed started to deliver clear signals of rate cuts ahead. The coast finally seemed clear for the banking system.

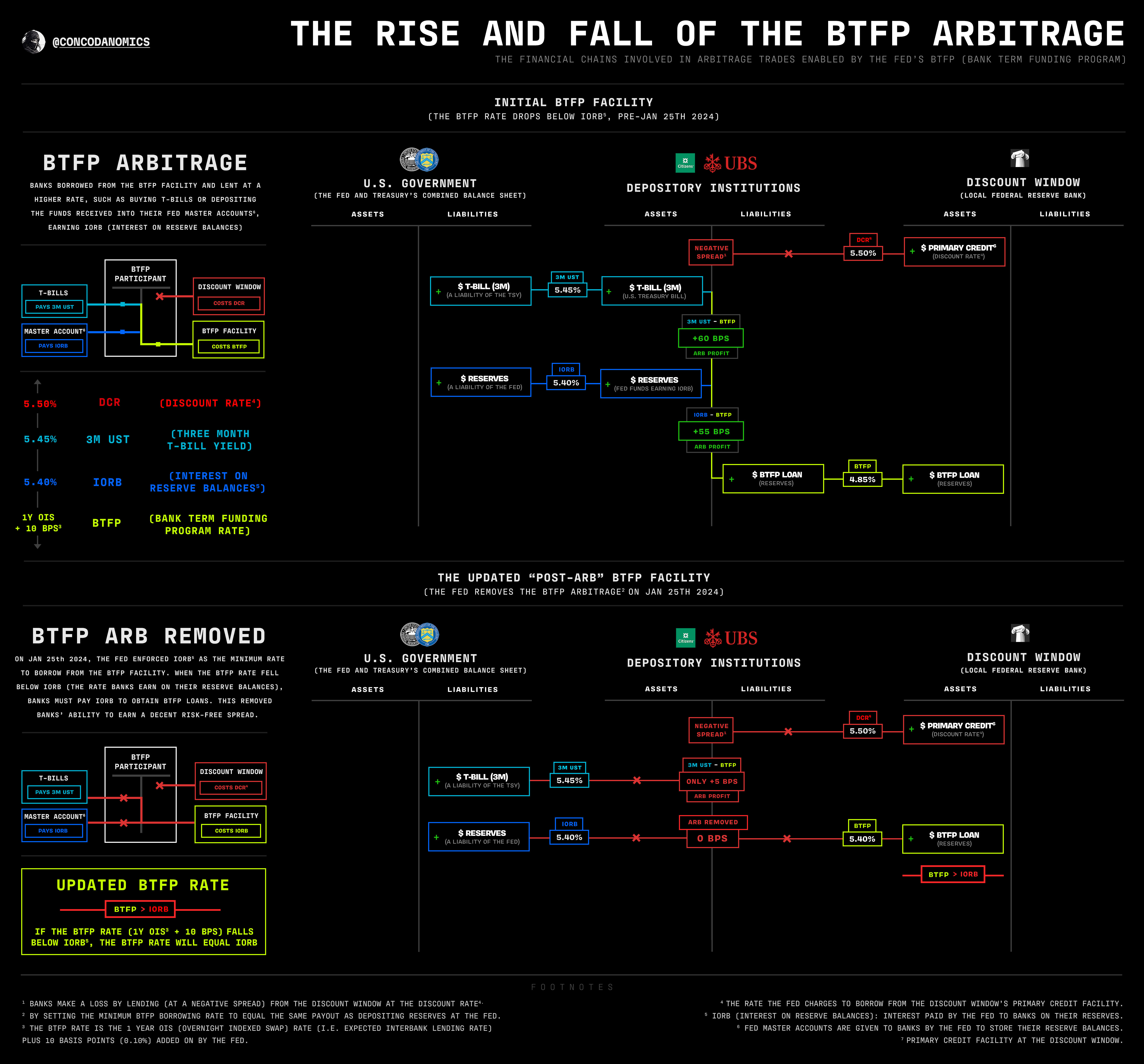

That was until volumes at the BTFP facility reaccelerated. But yet again, fears were misplaced. Increased usage delivered another false signal of impending ruin. Because Fed officials chose 1-year OIS (the 1-year overnight indexed swap rate, a forward-looking interbank borrowing measure) plus 0.10% as the cost to borrow from the facility, the BTFP rate plunged while several cuts were priced in. The BTFP consequently transformed from an emergency backstop into a risk-free arbitrage for banks, who started borrowing reserves cheaply from the facility to “lend” to the Fed at a higher rate of interest. This involved banks depositing reserves borrowed from the BTFP into their Fed master accounts to earn interest on reserve balances (IORB), profiting from roughly a 0.50% (50bps) spread.

Week after week, alongside a favorable economic outlook and some of the loosest financial conditions on record, arbitrage trades pushed BTFP volumes higher, peaking at around $170 billion outstanding. Then, on January 25th, 2024, the Fed suddenly revealed it would no longer accept new BTFP loans after the facility expires on March 11th, 2024. The U.S. central bank also killed the BTFP arbitrage, raising the facility’s minimum borrowing rate to equal IORB. This meant banks would earn 0% (0bps) on future trades.

Fast forward to today, the Fed and other monetary leaders globally have begun to fix the apparent flaws in their “lender of last resort” systems, the same systems in which the BTFP was established. Plans to construct an updated version of the Fed’s primary rescue mechanism are now underway. Let’s dive deeper.