The Treasury Market Dark Spot

modern-day markets are not only growing more complex but more opaque. that's a toxic combination, if left unchecked

As global markets slowly tumble while liquidity wanes, trillions of dollars present in the system are preventing any major unrest from developing in equity and credit markets. If significant turmoil is likely to emerge anywhere soon, it’s in America’s sovereign bond market.

After reaching levels not seen since the COVID meltdown, Treasury market volatility has somewhat subsided. But we’re not out of the woods just yet. Further rate hikes from the Federal Reserve could expose the underlying rot in the most important bond market globally.

Recently, after a succession of failed attempts, markets have made their first concerted effort to price in peak inflation. Energy commodities, gold, and even bonds have signaled disinflation, while sticky areas of the CPI (rent and wages) have shown early signs of a reversal.

This all followed the most disinflationary U.S. CPI reading since March, causing an explosive reaction in bond markets. A relentless bid in Treasuries kickstarted a lengthy decline in yields from ~4.1% to just below 3.5%.

Has a crisis been averted in America's sovereign debt market? Not so fast. Even if the Treasury market endures the stress of the remaining rate hikes now being priced in, long-term structural defects exist deep in its plumbing. New cracks in America’s sovereign bond market are beginning to emerge. After monetary officials have spent the last decade or so plugging every hole in U.S. money markets, it’s likely they will have to perform the same circus, this time in the U.S. Treasury market complex.

The Fed is already on call to supply unlimited liquidity to what Conks calls the REM Industrial Complex: the Repo markets, Money-market funds, and the Eurodollar market. These tools, however, will fail to quash other looming Treasury market hazards.

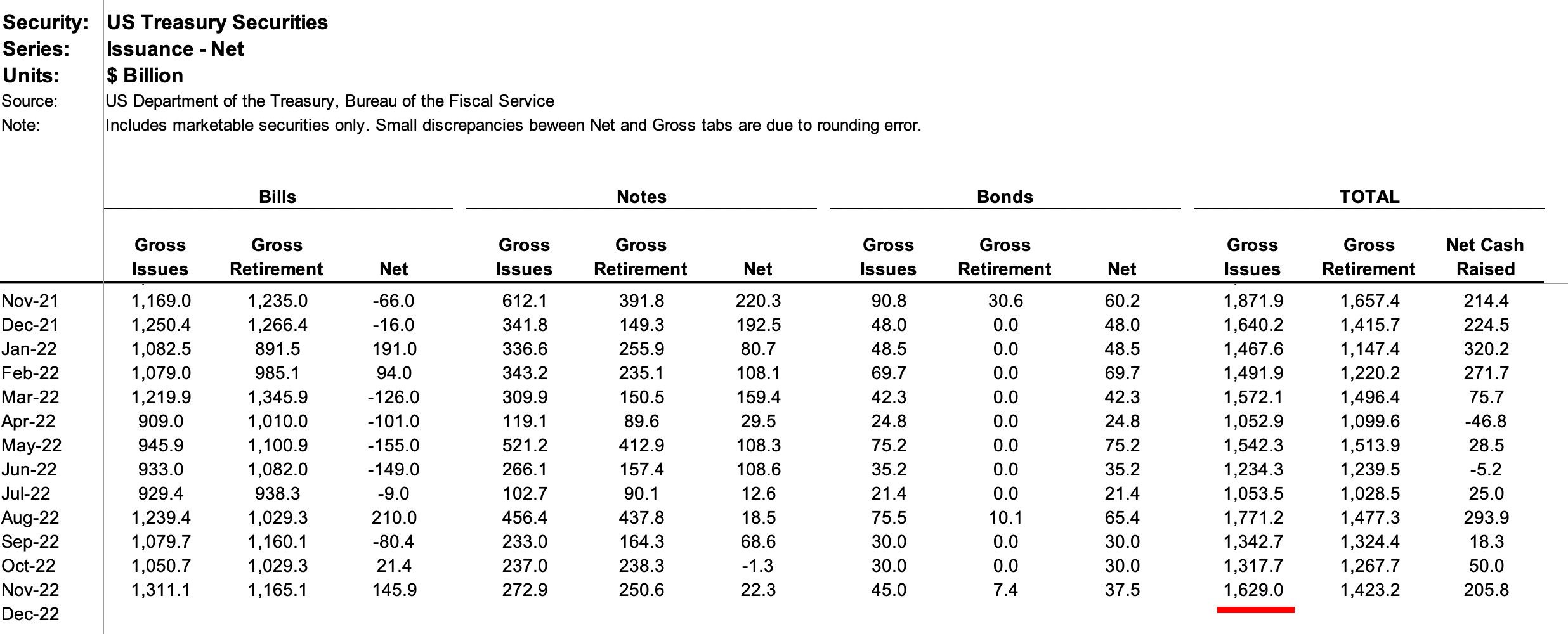

For now, the primary Treasury market, where investors simply buy bonds from the U.S. government, remains functional and liquid. The world can’t get enough of Treasury auctions, with a whopping ~$550 billion in net Treasury issuance expected this quarter.

The most prominent concern is that the most significant dealers in Treasuries (the Fed’s primary dealers and other large financial players) won’t be able to devour and intermediate an incoming 1 to 2 trillion dollars in Treasury issuance each year, which the U.S. government must “print” to fund its operations.

Luckily, the gap between the Treasury supply and potential buyers remains too slim for immediate concern. Plus, most of today’s trading exists in “on-the-run” Treasuries (a fancy term for the latest batch of government bonds issued), while off-the-run bonds are mainly held to maturity.

And even if liquidity problems develop, quick fixes like removing Treasuries and reserves from leverage ratios such as the SLR (Supplementary Leverage Ratio) can be used by officials. Primary dealers, the major plumbers in Treasury markets, can then absorb the colossal supply and offload it to buyers in secondary markets efficiently.

It is here, in the murky parts of the secondary Treasury market, that more short-term threats linger. Monetary leaders have finally begun to take notice of a system rife with structural issues, monopoly power, and, most importantly, blindspots. On the surface, the secondary Treasury market appears to be transparent and functional.

There’s the “interdealer segment” where firms (mostly securities dealers and specialized trading firms) trade among themselves automatically, using high-frequency trading algorithms. Then, you have the tiny dealer-to-dealer segment. This market facilitates the 10% of trades that occur directly between dealers without intermediation. This is because some parties want to execute large trades and not broadcast their positions to the wider market.

Finally, the most important part is the dealer-to-client segment. Participating in nearly every trade via specialized trading platforms, the Fed’s primary dealers and other firms make markets for foreign central banks, hedge funds, pension funds, corporations, and more.

Under the surface, however, notable signs of decay have emerged, ever since the infamous October “Flash Rally” of 2014. 10-year Treasury yields plunged 0.4% then swiftly rebounded for no apparent reason. Over five U.S. agencies failed to diagnose an actual cause in the aftermath.

Then, five years later in September 2019, rates in the repo (repurchase agreements) market soared. Some dealers were not authorized to use the discount window — which is the Fed’s emergency lending facility, so repo rates shot above the Federal Reserve’s target range following a cash shortage. The Fed responded by creating a “temporary” Standing Repo Facility (SRF).

Through primary dealers and the tri-party repo platform, the Fed offered the market unlimited cash loans at a rate they couldn’t refuse. Rates declined and normalized. And after realizing it patched a hole in the system, the Fed upgraded the SRF to a permanent installation.

A year later, the COVID-19 panic caused an epic market meltdown. Hysteria spread so widely that some investors couldn’t sell Treasury securities to raise U.S. dollars. Bid-ask spreads blew out, causing Conk’s “illiquidity spiral” to be exhibited in full force. The Fed soon stepped in as a lender (and now dealer) of last resort.

Soon after, COVID fears died down along with market panic. Monetary leaders and policymakers, however, suddenly woke up to the underlying deterioration in the secondary Treasury market. They began to try to fix its weaknesses, but this was easier said than done. An abundance of challenges awaited them.

Regulations like the aforementioned Supplementary Leverage Ratio (SLR), which have been developed to prevent a repeat of the 2008 financial crisis, can only do so much against emerging threats. These regulations have quashed old hazards but created new ones and added extra constraints. The Basel III Accords and Dodd-Frank have caused major financial behemoths (the Fed’s primary dealers and other large depository institutions) to pull back from risk-taking and market-making. JPMorgan has even closed its tri-party repo business because of regulatory penalties.

Today, other entities have taken market share. Slowly over time, unknown to most outside observers and even some policymakers, a new type of dealer has emerged behind the scenes: principal trading firms (PTFs). Their existence shows we remain in the golden age of monetary alchemy.

PTFs, firms that trade using high-frequency trading (HFT) strategies on state-of-the-art electronic platforms, have contested the big bank’s reign as the top market makers of Treasuries. Not constrained by the stringent rules applied to G-SIBs (global systemically important banks), PTFs have thrived.

They have joined other types of dealers who serve as the plumbers of the global financial system. By profiting off the spreads while trading Treasuries, MBS (mortgage-backed securities), and other securities, these monetary plumbers have created abundant liquidity worldwide.

These firms, though, are also slowly turning money markets into an increasingly complex and opaque beast. So much so that power structures are bound to take notice eventually. Large portions of the financial system are still covert.

Opaque markets decrease competition and increase costs, creating not only inequality but illiquidity. Opacity also allows big players to exploit smaller ones easily through monopolies on information.

The post-GFC (Great Financial Crisis) changes show us that a more transparent system fixes this. After “opacity” was blamed for AIG blowing up the CDS (credit default swap) market in 2008, the DTCC (the post-trade processor of OTC derivatives contracts) started publishing weekly data. Soon after, liquidity and competitiveness soared.

Monetary officials worldwide will aim to repeat a similar process for Treasury dark spots. And with this push for clarity, the Treasury market will start to transform. Monopolies do exist in these waters, and big players will likely not give up their thrones without a fight. A battle for control will brew between dealers with a monopoly on market info and regulators.

Even so, the authorities will likely win. And according to the consensus among commentators, academics, and monetary leaders, the plan is to combine the three Treasury market segments into one, turning it from an opaque, over-the-counter (OTC) market into an “all-to-all” behemoth. “All-to-all” is a form of trading that seeks to enable any participant in a market to trade with any other party — a model that is also the standard for stock, options, and futures exchanges.

Transforming the secondary Treasury market into an all-to-all model, however, will be a monumental task. Authorities, among other things, are asking private entities to reveal any suspect dealings or unfair market practices they could be engaging in.

But for regulators, the risks are becoming too large to watch on idly. It’s clear now that they have an incomplete view of what’s happening deep in the monetary plumbing. In the “uncleared bilateral” repo market, for instance, where trillions of dollars in bonds are pledged for cash to facilitate short-term loans, there’s limited oversight.

Uncleared bilateral repo (UBR), is one of the most elusive (and exotic) money markets. Its title sounds confusing, but it denotes the simple act of swapping securities for cash overnight for a fee, doing so anonymously — not using a central counterparty or custodian in the transaction.

With around $2 trillion in outstanding UBR agreements, the potential risks remain hidden. UBR dealings take place over the phone or through electronic chat, and participants determine what information they wish to divulge on certain trades.

Still, the authorities don’t seem to have (enough) urgency to stop trillions being traded in secrecy. After recent events in the U.K., this could be a perilous decision. Systemic risk abounds when financial entities go unwatched for too long. America’s Eye of Sauron™ looks to be diverted.

The reason they haven’t taken prompt action is the same as usual. Bureaucracies are slow to react to monetary threats and usually end up imposing emergency measures — some of which turn into conventional monetary policy. In February 2022, the Treasury’s Office of Financial Research (OFR) did announce it would pursue a permanent collection of data for UBR trades. The new collection would complement other sources collected by regulators on cleared and tri-party repo. But this, even after recent affairs, has yet to be completed. Time is ticking.

Once implemented, authorities will gain more oversight over dark parts of the repo market. But they won’t stop there. Conks predicts they will then try to centrally clear all trades that involve Treasury securities. Only last month, officials from five agencies vowed to change the system so that the majority of trades went through CCPs (central clearing corporations).

Central clearing is said to be the string that will form a new web of financial transactions. As the flow of funds from a fictional dealer demonstrates below, trading through CCPs looks intricate and complex. Yet it provides numerous benefits for those who participate.

Once most participants onboard to CCPs, this will create more transparency, increase efficiency, and reduce systemwide risk. Instead of dealers taking heavy losses and sparking contagion, the CCP insures its members against the default of other members. Each participant in the clearing process must deposit “clearing collateral” and also contribute a specified amount to the CCP’s “default fund”.

This allows the CCP (not the Chinese Communist Party) to offer three layers of protection before “contagion” even becomes a problem. If a member defaults on a trade, it first gives up any pledged collateral to cover losses, followed by its contribution to the CCP’s default fund. If that’s still inadequate, the CCP uses its capital to settle the loss. Plus, in extreme situations, other members’ funds will be used to settle losses. Conks calls the entire process “the waterfall of pain”.

As you can see, these are just some of the tools that exist to create a more transparent, open, and resilient American sovereign bond market. Monetary leaders will eventually need to act, and perhaps somewhat quickly. But judging by history that won’t happen. They’re aware but unhurried. The Treasury Market Practices Group (TPMG) not only admitted that the clearing and settlement process is “fragmented”, but capital flows may not be understood by some participants who “lack a clear and comprehensive view of market functioning.” Their words, not ours.

It’s hard for anyone to find an optimal solution to the problems that leaders face with the Treasury market, let alone the global financial system. It’s grown so complex, with endless moving parts and incentive structures, finding a true “fix” has grown impossible. But after 2008, a subprime-style house of cards must be prevented from emerging in the financial plumbing. Efforts to improve Treasury market functioning and transparency to identify dangers have begun from both state agencies and the private sector. Failing to identify a serious hazard in the Treasury market before it’s too late will cause a further tumble in the public’s already fragile confidence in policymakers and institutions. This time, there’s no room for error.

If you enjoyed this, feel free to smash that like button and share a link via social media. Thanks for supporting macro journalism!

“Failing to identify a serious hazard in the Treasury market before it’s too late will cause a further tumble in the public’s already fragile confidence in policymakers and institutions”.

Yep. I can summarize this article in two words ‘money laundering’. And those of us putting in the sweat to pay both the visible and hidden taxes are DONE with it. Just my uneducated opinion

Does this cross refer to what the BIS just raised as a big concern for them? There feels like a disconnect between your, ‘the fed has more tools than you can imagine’ POV and this nightmare when combined with the off financial statements trillions the BIS talked about. Genuinely asking and not looking to point score