Plumbing Notes: It's Not QE

the mechanics behind the Fed's coming balance sheet "bazooka"

Money Market Commentary

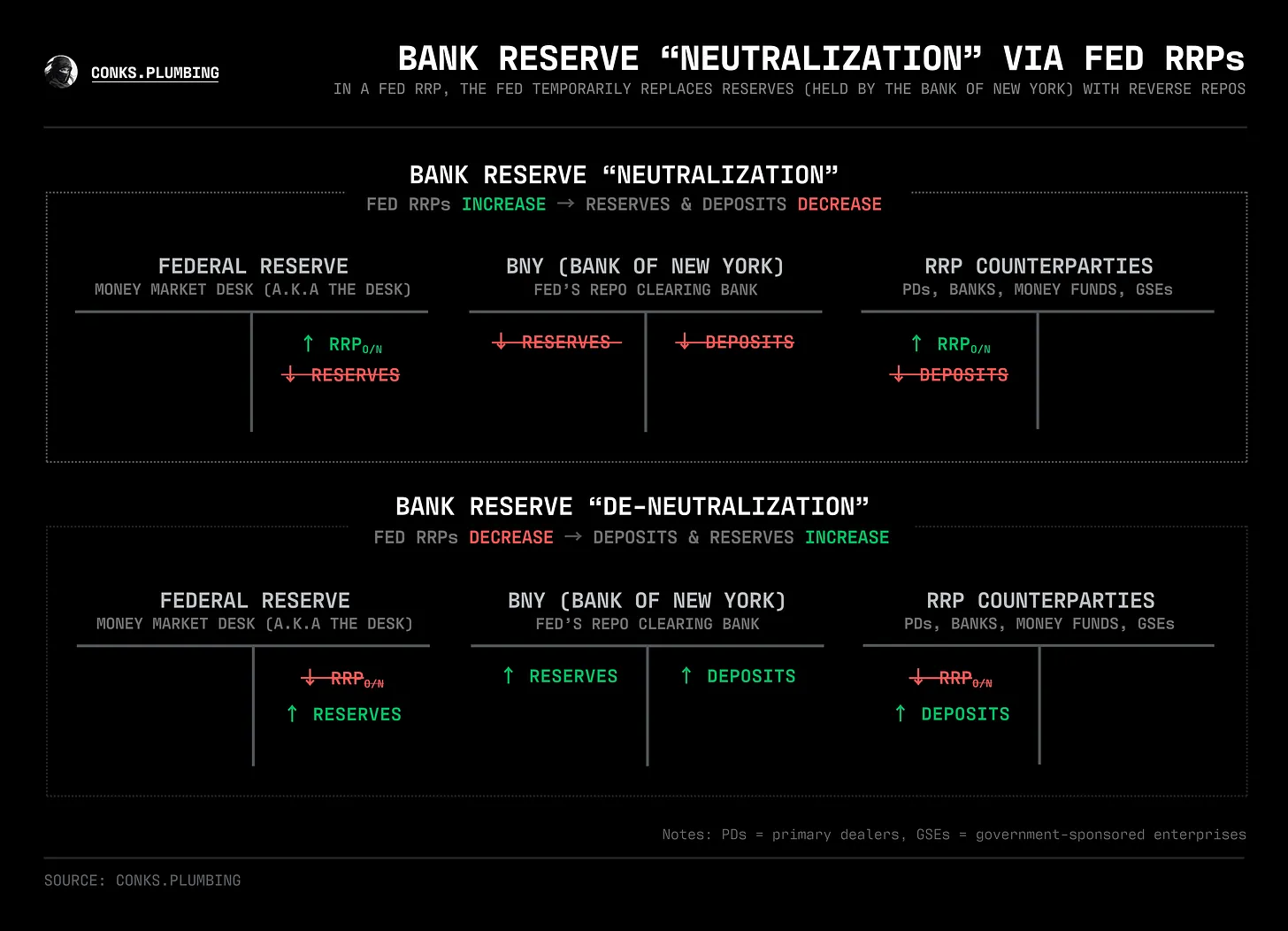

The Fed’s plumbing put awaits, with the U.S. central bank set to expand its balance sheet once again. Even so, monetary leaders initiating RMOs (reserve management operations) will likely unleash more flawed takes on “liquidity” than stimulate financial markets, let alone the real economy. What the Fed is about to unleash isn’t QE (quantitative easing), stealth QE, or even stealth easing. These involve the Fed swapping reserves for safe assets (USTs), absorbing duration risk in the hope that the private sector liquidates its most risky assets and spends into the real economy. This time around, monetary leaders will merely boost reserves to offset forces outside balance sheet runoff (i.e. QT) that will eat away at banks’ reserve balances and potentially (but unlikely) induce “repocalypse” 2.0.

“RMOs” (reserve management operations) better describe what the Fed is about to undertake, namely boosting banks’ reserve levels, which will continue to wane, even with QT no longer in effect from December 1st. Despite the Fed’s balance sheet runoff ceasing, interbank liquidity will slowly wither away by either temporary or “permanent” means. Reserves can be temporarily removed (i.e. neutralized) from the banking system via an increase in overnight (o/n) Fed RRPs, or from foreign central banks investing their overnight dollar liquidity in the Fed’s FRP (foreign repo pool).

{kind=link}