While news of the U.S. dollar losing its supremacy has been spreading quickly, behind the scenes, America’s monetary leaders have been taking steps to reinforce the Greenback’s global hegemony. Now, with the Federal Reserve’s “final frontier” in operation, the dollar’s grip is about to grow stronger than ever.

Since the Great Financial Crisis (GFC) of 2008, the Federal Reserve has operated a system, not built on sound pre-planning, but on its responses to a seemingly endless number of crises in increasingly complex markets. Its decision to flood the financial system with bank reserves shattered the existing mechanism for setting interest rates, sending Fed officials on a journey to implement a fresh monetary regime: The price of money (interest rates) would no longer be set by the Fed altering the number of reserves in the system but by implementing a set of rates. The result? The gradual emergence of the Fed’s “global jaws”.

First came the Fed’s initial upper jaw in 2008. On October 6th, shortly after the fall of Lehman Brothers, the Fed started paying interest on reserve account balances, most of which belonged to the big Wall Street banks. Named IORB or “interest on reserve balances”, this rate acted as an anchor on Fed Funds, holding it — and other short-term money market rates — within the Fed’s newly established target range (as seen below in navy blue).

Though a significant change, paying interest on bank reserves was just the start of the Fed’s jaw construction. Soon after, officials began assembling a soft lower jaw: a tool to nudge falling money market rates, including Fed Funds (EFFR) and short-term Treasury yields, back into its target range. In late 2013, with both rates and yields near zero and approaching negative territory, Fed officials grew worried, not only about yields on Treasuries turning negative, but that when the Fed hiked for the first time since the GFC, raising the IORB rate (the Fed’s upper jaw) was sufficient to drive short-term rates higher. The Fed reacted swiftly, implementing an overnight reverse repo facility, commonly known as the RRP. This allowed certain banks, money market funds, and GSEs (government-sponsored enterprises, like Fannie Mae and Freddie Mac) to lend to the Fed at its overnight repo rate (ON RRP). By increasing ON RRP, the Fed could raise short-term rates whenever it deemed necessary. Its soft lower jaw was now in operation.

{kind=link}

The initial versions of the Fed’s upper and lower jaws, however, were defective and incomplete. Still to surface were various disruptive episodes, which would come to remold their initial structures. After the infamous “repocalypse” of September 2019, the Fed introduced the standing repo facility (SRF), setting a hard ceiling on repo rates. Entities borrowed cash at the standing repo rate (SRFR), bypassing higher private borrowing costs, which restored balance in markets. A few years later, the COVID market meltdown showed that the Fed required a permanent global backstop. Monetary leaders reintroduced official central bank swap lines, fortifying the Fed’s upper jaws. Still, the Fed’s job wasn’t done.

{kind=link}

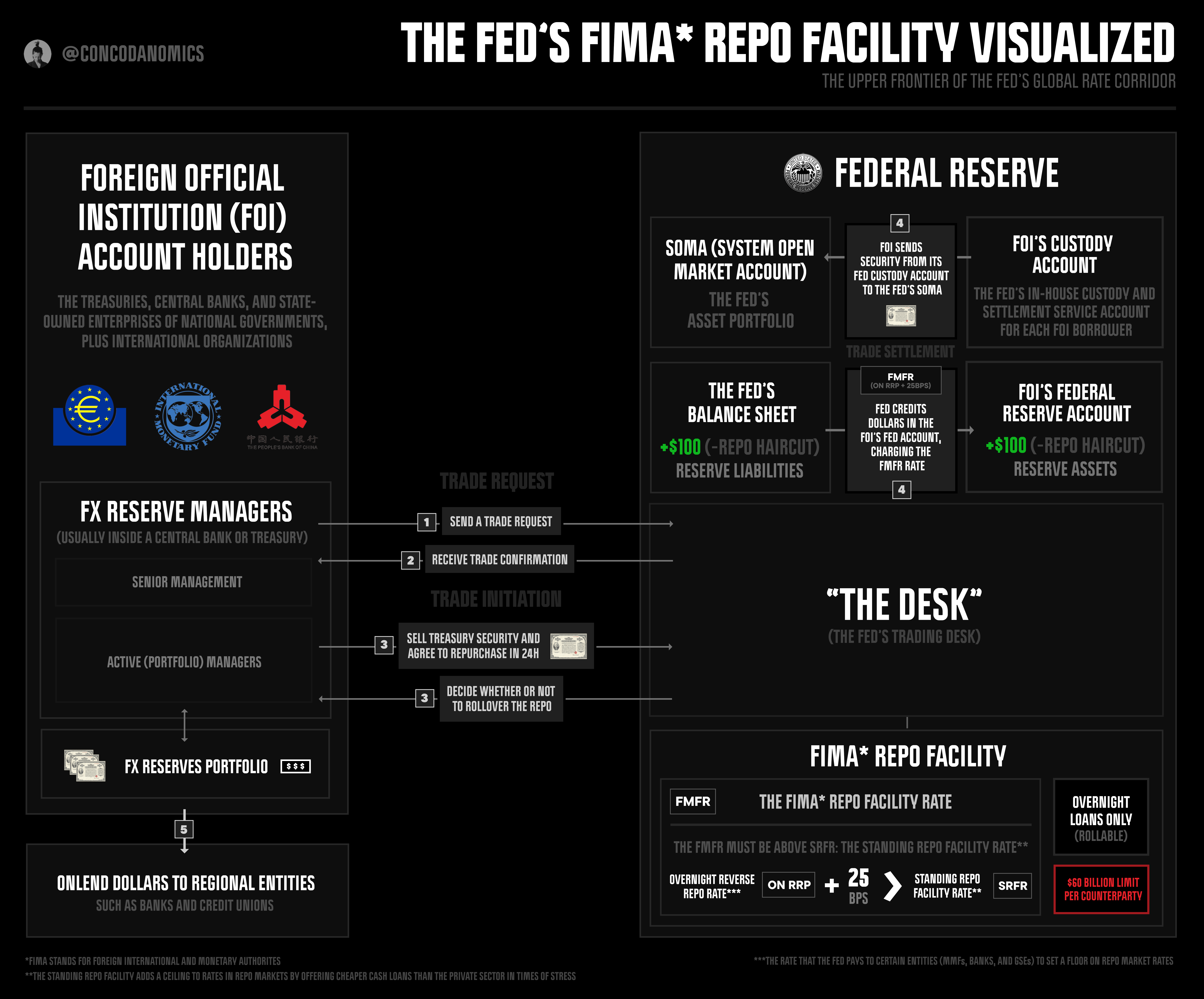

The volatility of COVID-19 was so extreme that it threatened the stability of public institutions’ dollar portfolios. Struggling with a volatile atmosphere, foreign official institutions (FOIs) — namely the treasuries and central banks of foreign governments plus international organizations — were on the brink of firesaling U.S. Treasuries and other dollar assets to raise cold, hard cash. Before a governmental-level calamity ensued, the Fed stepped in, adding another layer to its global jaws. The FIMA repo facility, the Fed’s “final frontier”, was born.

Alongside the private dollar ceiling of swap lines, a public dollar ceiling was about to provide America’s allies and rivals with another safety mechanism in times of crisis. Yet it would also increase the world’s reliance on the U.S. dollar and its many derivatives. What did this look like in practice? Let’s go deeper into the mechanics.