Plumbing Notes: Statecraft & the TGA

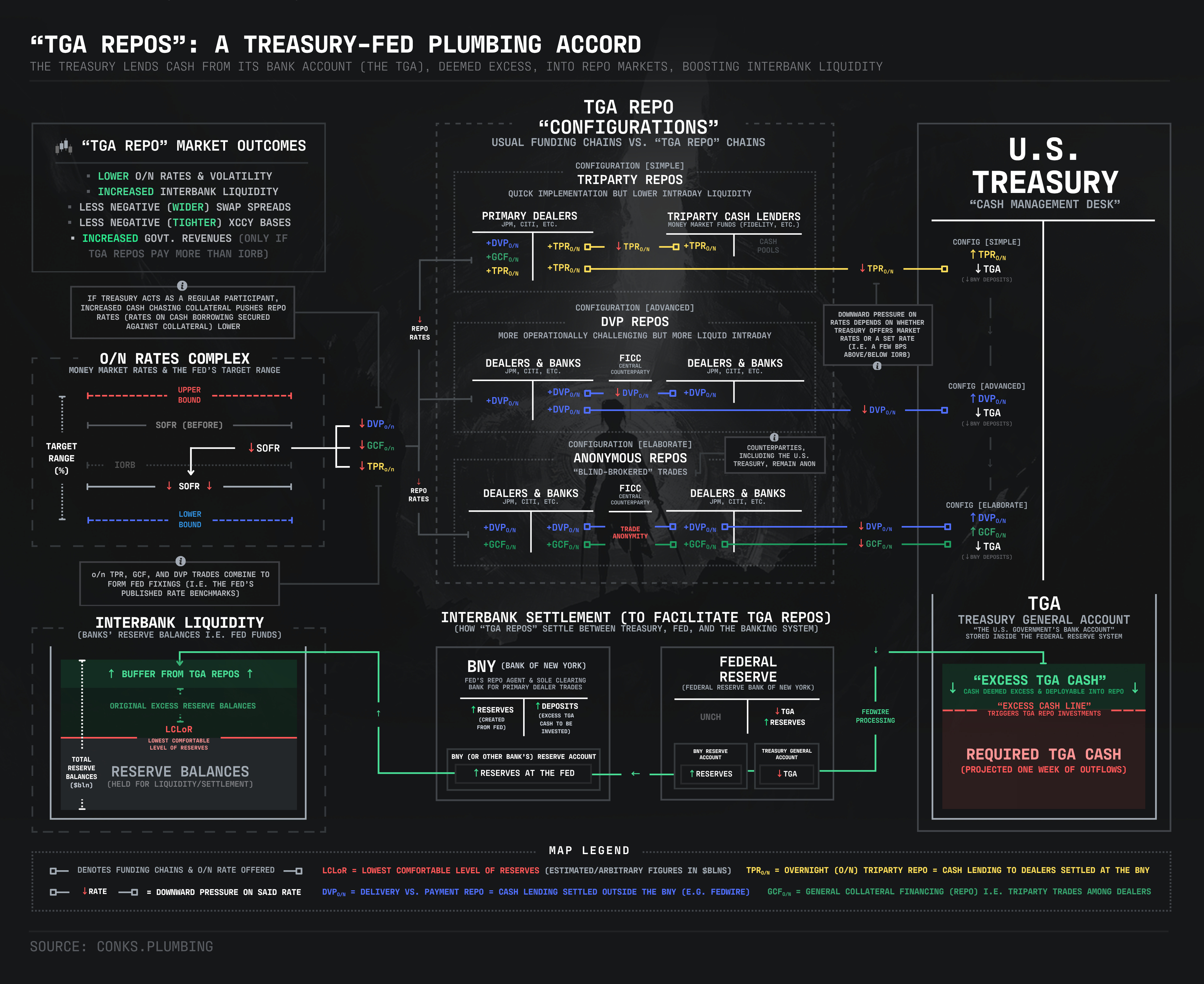

a new type of Treasury-Fed accord is looming

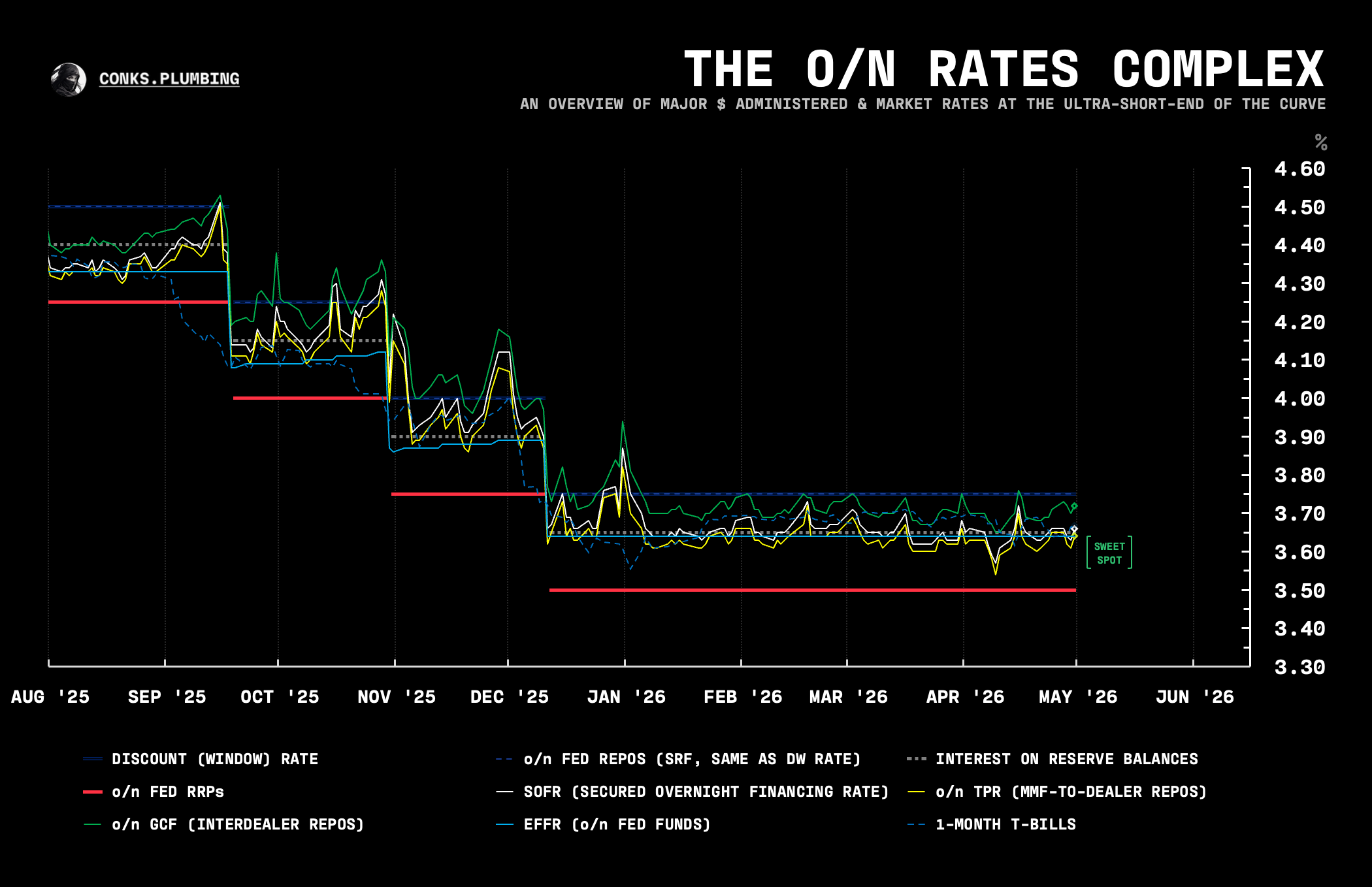

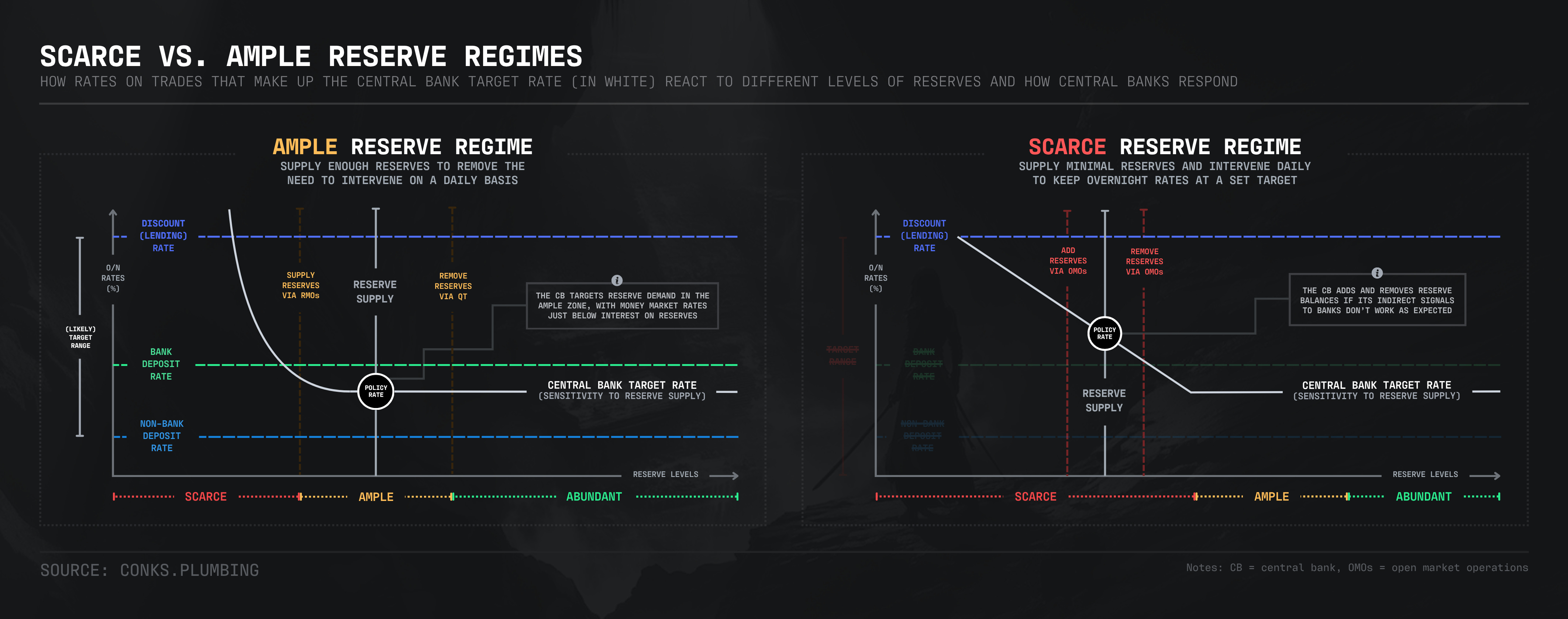

The level of monetary statecraft continues to climb. Causing a “stir” on the street, TBAC — a group of private-sector thought leaders that advise the U.S. Treasury — announced a potential mechanism to deploy excess liquidity from the U.S. empire’s bank account, a.k.a the TGA (Treasury General Account), into U.S. money markets. From a sharp inflow of tax payments to a full-blown market panic, the level of TGA cash1 occasionally rises so sharply that it risks provoking2 another repo upheaval, where every rate forming the o/n (overnight) complex breaches the Fed’s upper bound. In the excess-cash era — created through the post-COVID flood of interbank liquidity injected through QE, a hundred-billion-dollar plunge in bank reserves failed to disrupt the U.S. central bank’s current ample reserve regime.

{kind=link}

But after the Fed’s destruction of trillions of dollars in excess reserves, the game has changed. A multi-billion interbank swing could decrease levels enough to reach the system’s dreaded lowest comfortable level of reserves (a.k.a LCLoR). Still wanting to prevent another money market disruption3, financial thought leaders have devised a plan to impose a new Treasury-Fed plumbing accord, via the creation of “TGA repos”.

By Conks’ estimates, reserve balances lie only ~$250 billion, a common swing in the U.S. empire’s cash balance, above the “danger zone”. Meanwhile, the TGA often continues to accumulate a mammoth “excess” buffer, above even the week of outflows the U.S. Treasury targets. A TGA repo “market” could thus provide an offset, becoming the mechanism to avert the next money market uproar. Yet barriers remain.