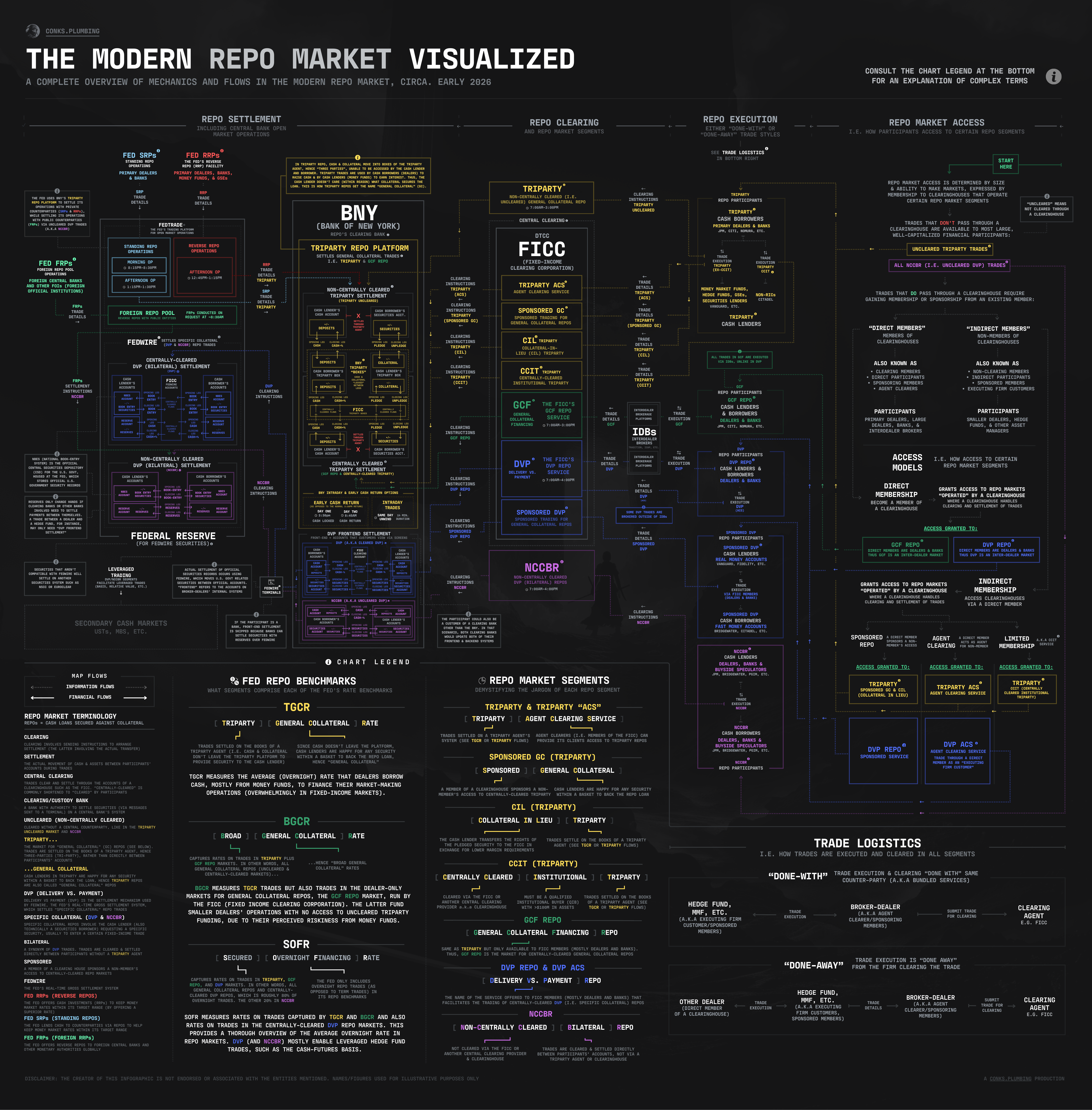

Recently, we published a “mega-infographic” that unveiled the plumbing of the repo market in detail.

Given the amount of information required to demonstrate the complete flows of a repo trade, the graphic is tough to navigate without a PDF version. Subsequently, we’re providing one for all readers below.

Still, even with complete visuals, a written explanation is needed to comprehend such an intricate ecosystem. Welcome to a Repo 101: a brief primer that will complement Part II of our current target rate series, covering repo lingo and mechanics in plain English. This is not the usual Conks style of article. Instead, it’s written to clarify all key repo fundamentals and rates as concisely as possible.