Plumbing Notes: Swifter Injections

the Fed is priced to pull the trigger sooner rather than later

— view our SOFR-FF primer and glossary for a better understanding of this topic. Let’s dive in…

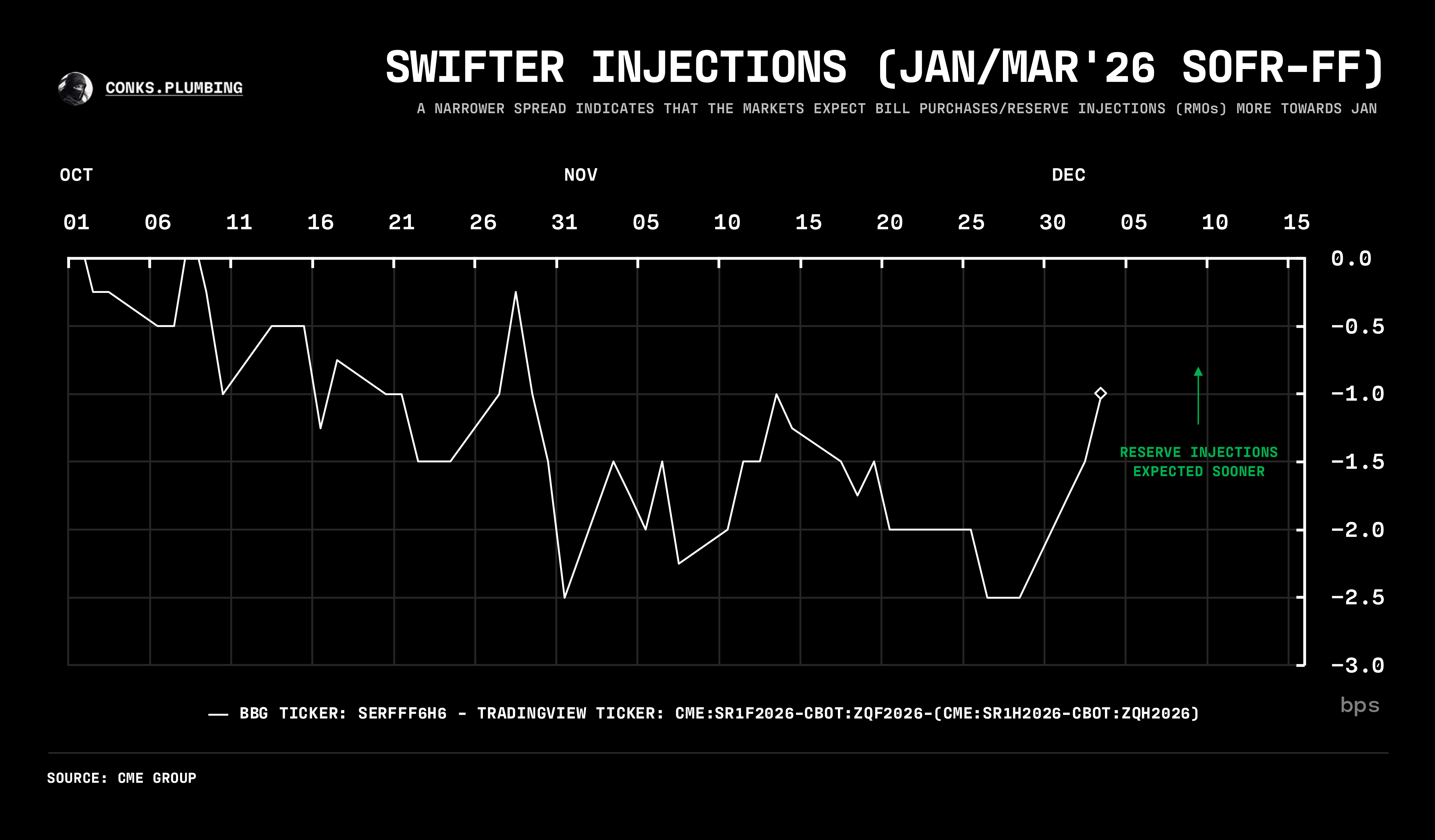

Reserves may arrive sooner than expected. The market has priced out delayed liquidity injections from the Fed, with an earlier balance-sheet expansion baked into markets. Trading desks now expect the Fed’s RMOs (reserve management operations) — where it buys bills with newly minted reserves to maintain ample liquidity1 — to begin closer to January.

This is observable via relative SOFR-FF (basis) spreads, which provide a contrast of dollar funding conditions at various points in time. Since SOFR-FF spreads rise (or grow less negative) when the market believes the SOFR-FF basis will narrow in one month compared to another, the latest market moves show traders are betting on earlier RMOs. They could be pricing in a multitude of catalysts. Nevertheless, SOFR-FF in Jan’26 tightening compared to March ‘262 likely suggests participants desire a swifter end to tighter money markets.