Plumbing Notes: The Equity Repo Mania

volatility has emerged in the most esoteric $ funding market

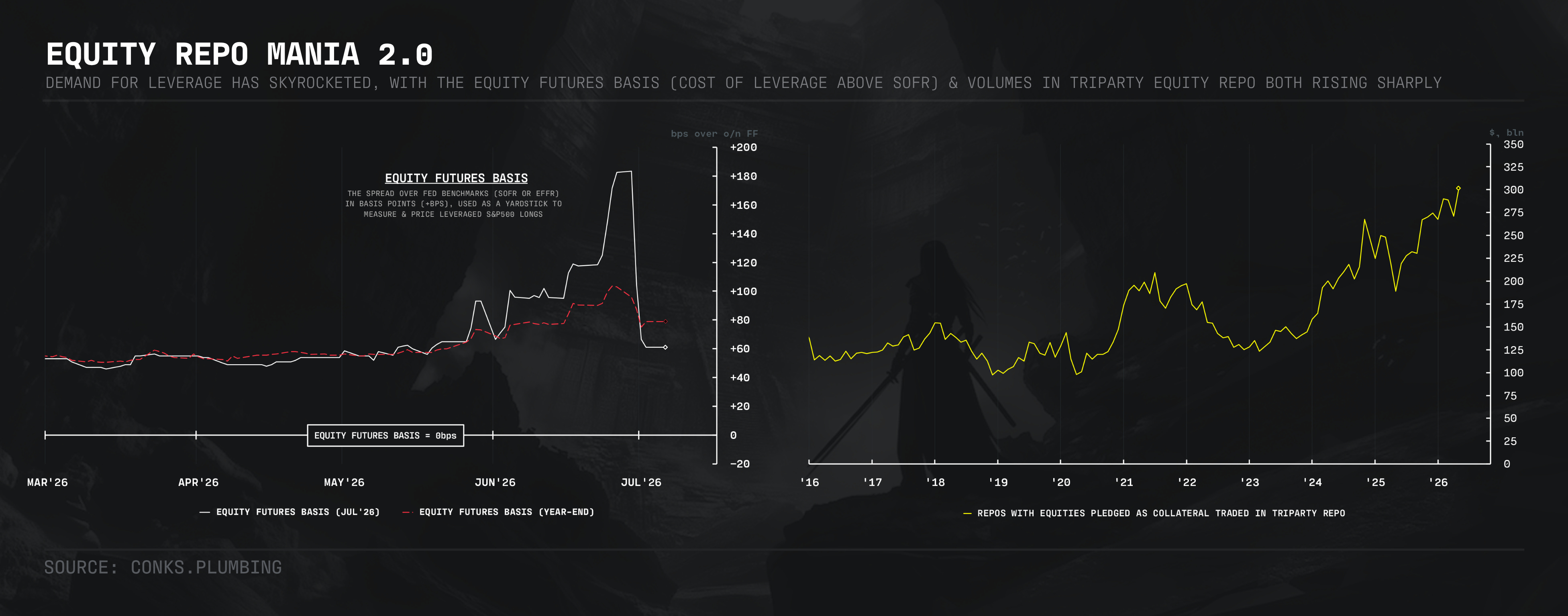

As broader money market rates have undergone a Great Compression, rates in the most mysterious part of $ funding markets have grown volatile. Known collectively as “equity repo”, the ecosystem for funding leveraged stock market exposure1 has seen funding rates take off and land. The largest dealer banks have experienced a massive influx of demand, followed by an epic pullback. A growing appetite for leverage amid soaring prices, along with a rising market cap, had increased the quantity and size of equity baskets (such as the S&P500) that primary dealers somewhat reluctantly had to finance. Paired with a certain IPO2, leveraged ETF boom, and AI meltup, balance sheets, for a short time, grew overloaded. Rates charged by dealers to facilitate equity repo trades even surpassed year-end levels3.

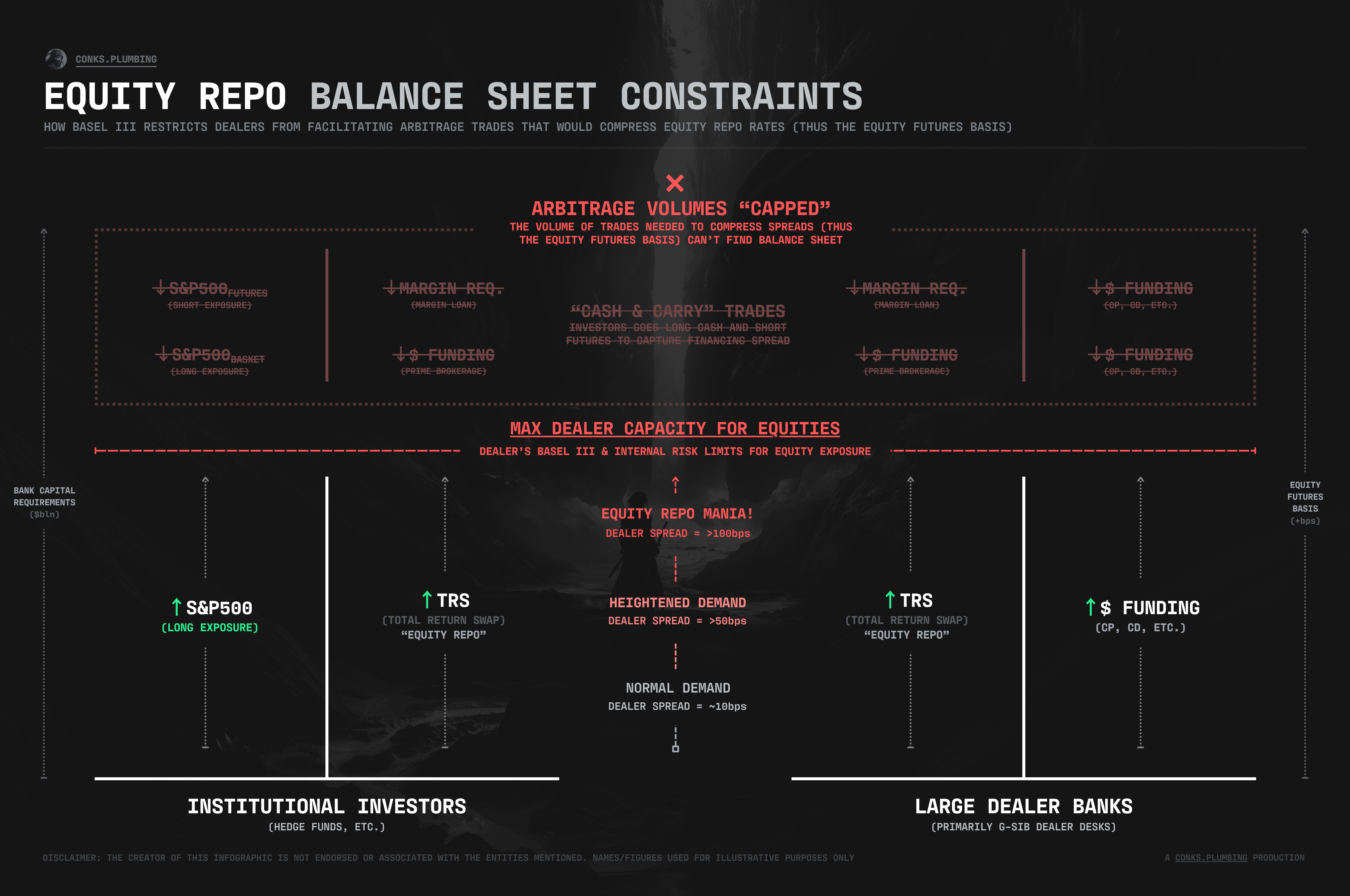

During the same period, potential rate hikes have replaced cuts, reducing demand for U.S. sovereign assets and influencing rates at which $ funding markets clear. Equity and bond market moves have thus been affecting the o/n (overnight) rate complex to the point that traders should take notice. The U.S. bond markets’ influence on $ funding markets has been well documented and priced in by most players. The impact of equity market leverage on $ funding markets, however, remains obscure. As each dealer possesses unique in-house funding rates and keeps them under “lock and key”, traders can rely on only one public measure to estimate appetite for stock market leverage: the “equity futures basis”4. By capturing the difference in rates between borrowing U.S. dollars in money markets (such as SOFR and o/n FF) and the average rate to provide the “total return” of stock market indices5, the equity futures basis has unveiled a mammoth thirst for levered longs6 provided by dealers with limited balance sheet7.

Forever constrained by Basel III, banks over the past few weeks have been compelled to charge +150bps above SOFR to supply stock market leverage, with the average rate surpassing even that of the last “mania” in late 2024.

As was the case back then, hedge funds have become willing to pay any price to obtain equity exposure, with little to no backlash. Consequently, “equity repo” has the potential to produce $ funding stress further afar.