Plumbing Notes: War & Short-end Rates

the ultra-short-end has become the new safe haven

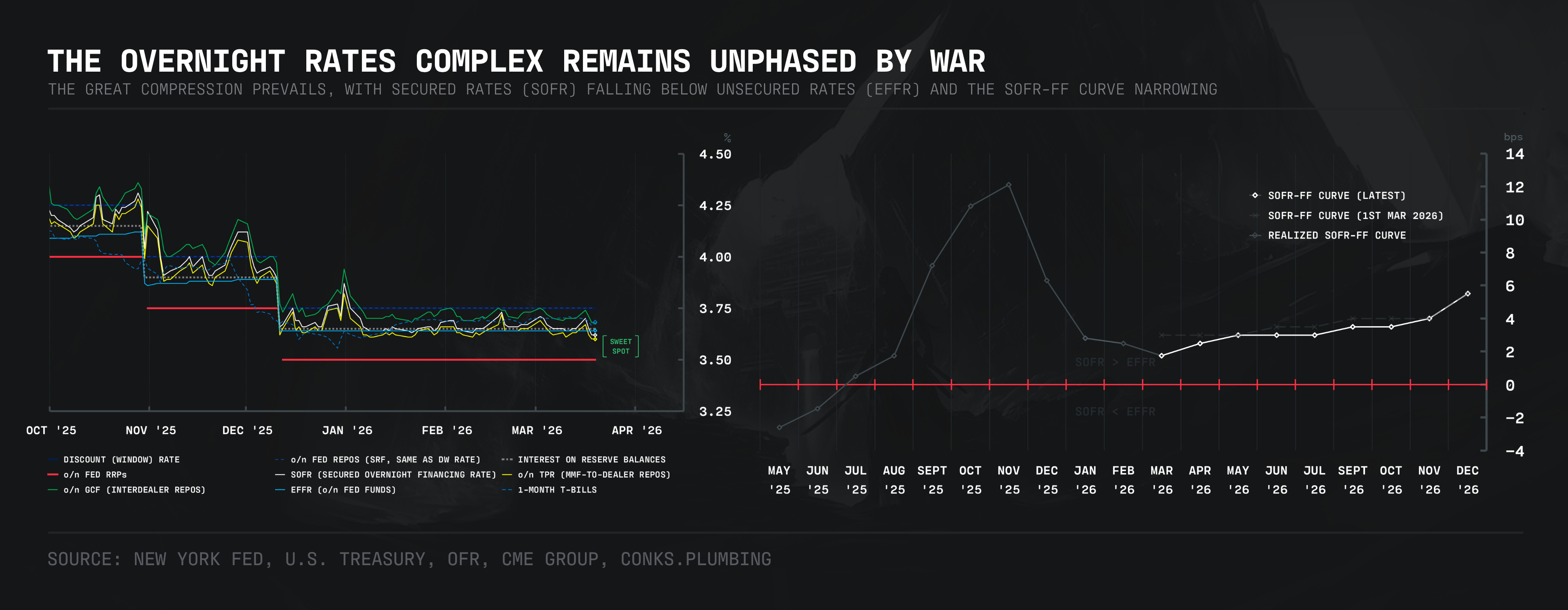

In the face of a prolonged Not-War, short-end rates and beyond continue to rise. The longer the Strait “that must not be named”1 remains closed to traffic, commodity prices will not only climb but persist at higher levels, feeding into both rates and risk via the pricing out of cuts and pricing in of hikes. Rates at the ultra-short-end2, meanwhile, have resumed their descent. Investors have rotated into shorter-term assets of the sovereign while exiting riskier sectors3. Increased bond market volatility has prompted further flows into money markets, as investors raise cash and take refuge in money market funds. The mini-cash flood has consequently helped push repo rates (SOFR) below even unsecured rates (o/n FF), expected in theory4 but not in the Basel III era. The Fed’s RMOs (a.k.a reserve management operations) have likewise suppressed o/n rates while forming a barrier against an incoming TGA-induced5 vacuum on April 15th (tax day), an obstacle that participants have subsequently6 priced out. The Great Compression, as indicated by money market pricing, remains intact.

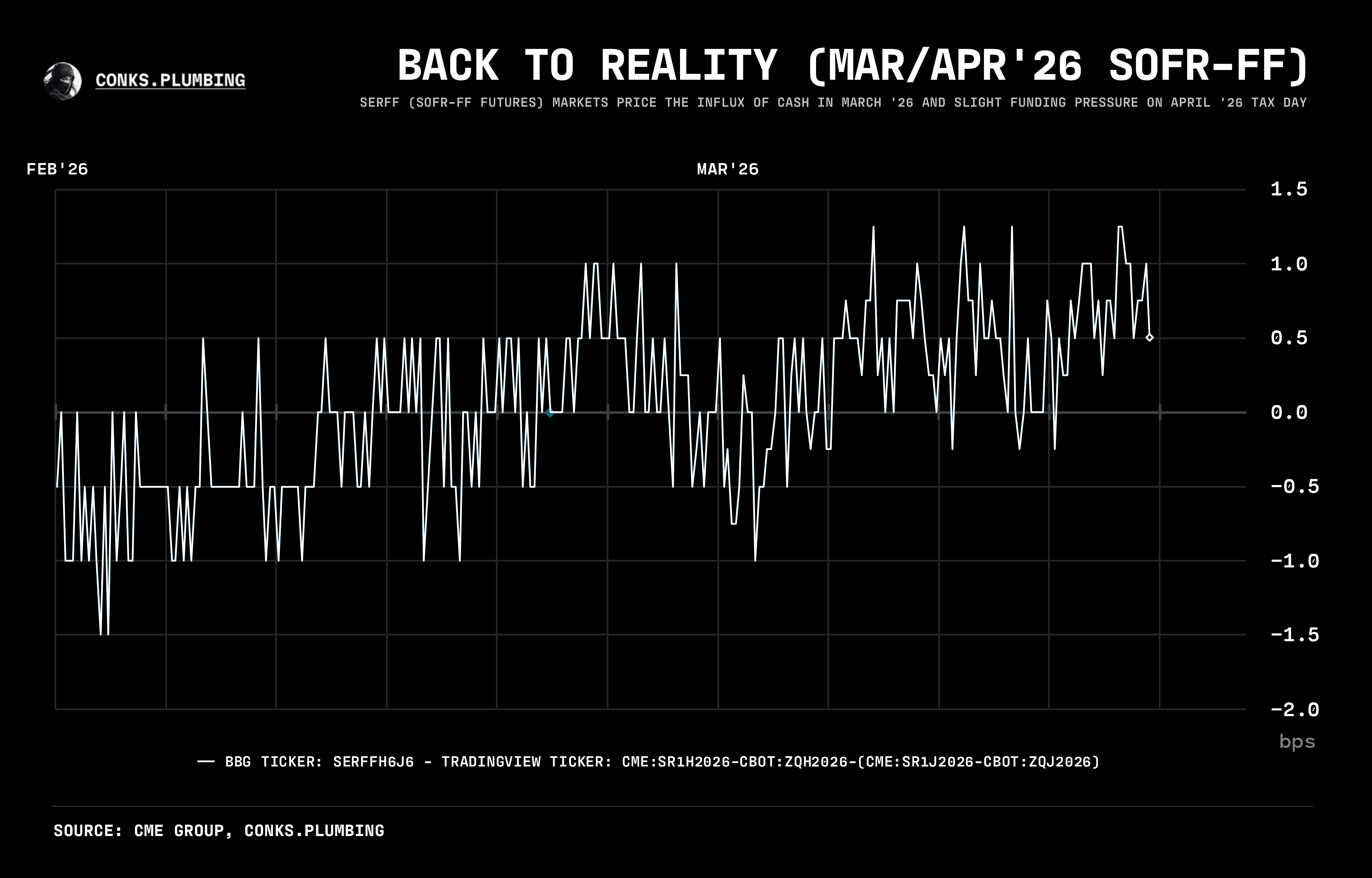

Markets exposed to a potential tax day blind spot7 have overlooked the now-low risk of a squeeze and respected the near-abundance of cash seeping into repo markets, evidenced by Mar/Apr’26 SOFR-FF8 (below) turning positive. As for the rest of the SOFR-FF curve, further compression is possible but will result in slim pickings for traders. For more significant moves, they must venture into stormier regions.

Volatility, thus opportunity, lies outside the comfort of o/n (overnight) markets. As laid out in War & Plumbing, a longer battle is more likely than a quick resolution, with conflict extending beyond late April resulting not just in zero rate cuts but also hikes9, ex-U.S. Despite what POTUS declares via social media, no true TACO remains on the table.