The Fed's Relief Valve: Part II

an attempt to grease the Treasury market's plumbing may fall short

— click here for Part I and here for Pro

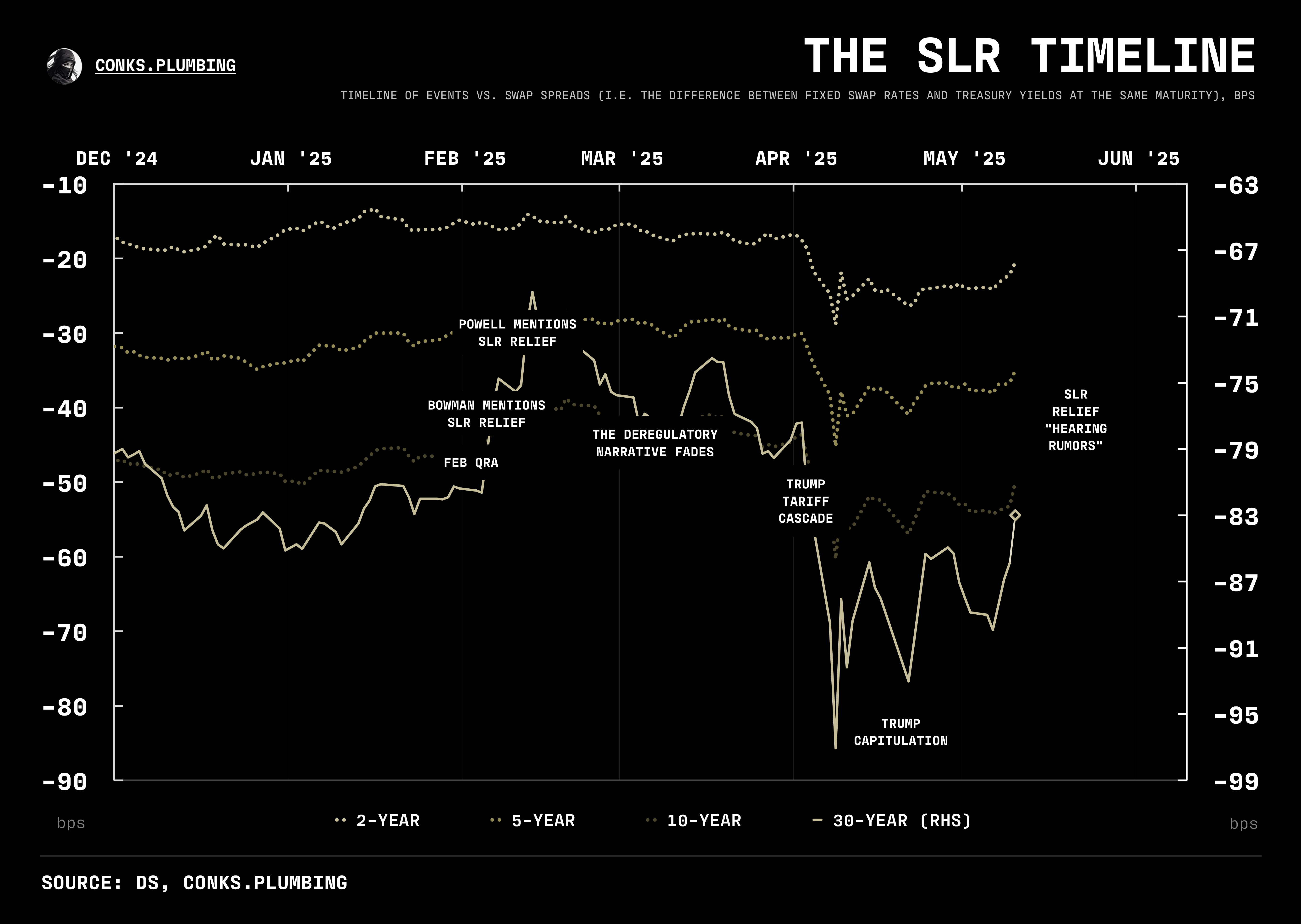

The hype over the Fed opening its “relief valve,” an easing of constraints impeding the largest UST (U.S. Treasury) market makers, has reached its peak. From a slowing of the Fed’s QT to officials hinting at a relaxation of dealers’ shackles, numerous catalysts briefly prompted markets (i.e. swap spreads1) to price in a “plumbing liberation”, one set to grease the Treasury market’s inner workings. This move, however, was quickly superseded by a regulatory “rug pull”, a sharp reversal in swap spreads spurred first by the longstanding pressures weighing on U.S. sovereign debt, plus a significant unwind in positioning. Panic produced by Trump’s “tariff cascade” then dealt the killing blow, as market participants began to genuinely question U.S. Treasuries as a global reserve asset. Desks engaging in key trades2 that fuel UST liquidity encountered mild stress, while long-end bid-ask spreads somewhat widened. The multipolar world and dollar doom narratives appeared (somewhat) feasible for the first time in decades.

But Trump’s capitulation to bond market volatility soon followed, prompting market participants to turn their focus back toward an incoming deregulatory agenda. An increasing number of leading officials have suggested easing the Fed’s SLR as the U.S. central bank’s primary relief valve mechanism. Nevertheless, this and other proposed modifications will fail to grease “the pipes” of the Treasury market as much as they anticipate. Numerous pressures, both political and technical, will continue to impede the UST plumbing.

Swap spreads, or simply “spreads” in market lingo, which directly capture the tenacity of dealers’ regulatory constraints, have adapted accordingly — downwards. A bigger Fed relief valve is needed.

{kind=link}