Plumbing Notes: Nothing Ever Happens

the softening of $ funding rates continues

The dampening of money market volatility has prevailed. Marked safe from geopolitical risk, o/n rates in repo, FX swaps, and unsecured dollar markets have settled at a new equilibrium or continued their descent. Multiple catalysts endanger such stability, but opposing forces are set to contain any notable pressures. The “nothing ever happens” idiom of equity markets has thus spread to the $ funding arena.

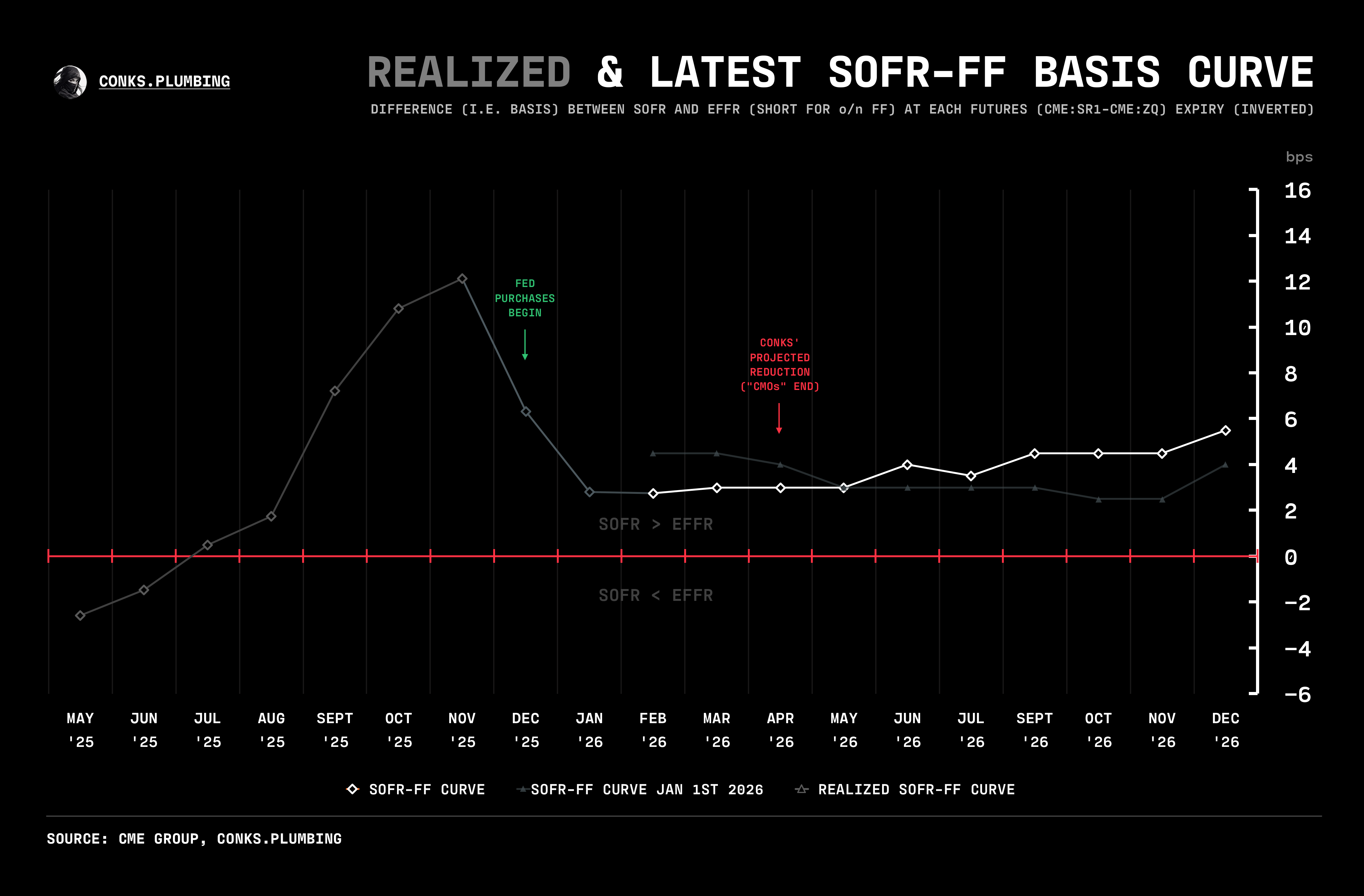

While repo rates continue to decline, higher interbank volumes have reduced the odds of o/n FF (a.k.a EFFR) printing lower, preserving a narrower1 SOFR-FF basis.

Swap spreads, meanwhile, may have widened (i.e. grown less negative) significantly, signaling easier plumbing conditions. Nevertheless, they could rally further. Fed proposals advocating for increasingly loose bank regulation should emerge by the end of Q1 this year.

As is evident, the Fed’s swift suppression of volatility has transformed money markets for better or worse, depending on the participant. It’s good news for U.S. monetary leaders who’ve compressed the overnight (o/n) rates complex to recent all-time lows, but bad news for some STIR traders starved of both volatility and thus opportunity. After the demise of the Fed’s QT, the Great Compression — i.e. a further narrowing across the SOFR-FF curve, post the Fed concluding its balance sheet reduction and starting reserve injections a.k.a RMOs — has been the only prominent trade. As anticipated, a few relative value plays have also emerged, based on the timing and size of the upcoming reduction in Fed purchases. But none offer, in Conks’ view, sizeable risk-versus-reward. Market participants must look further afield.