Plumbing Notes: The Fed's Overshoot

a cash flood may prompt a pause in liquidity injections

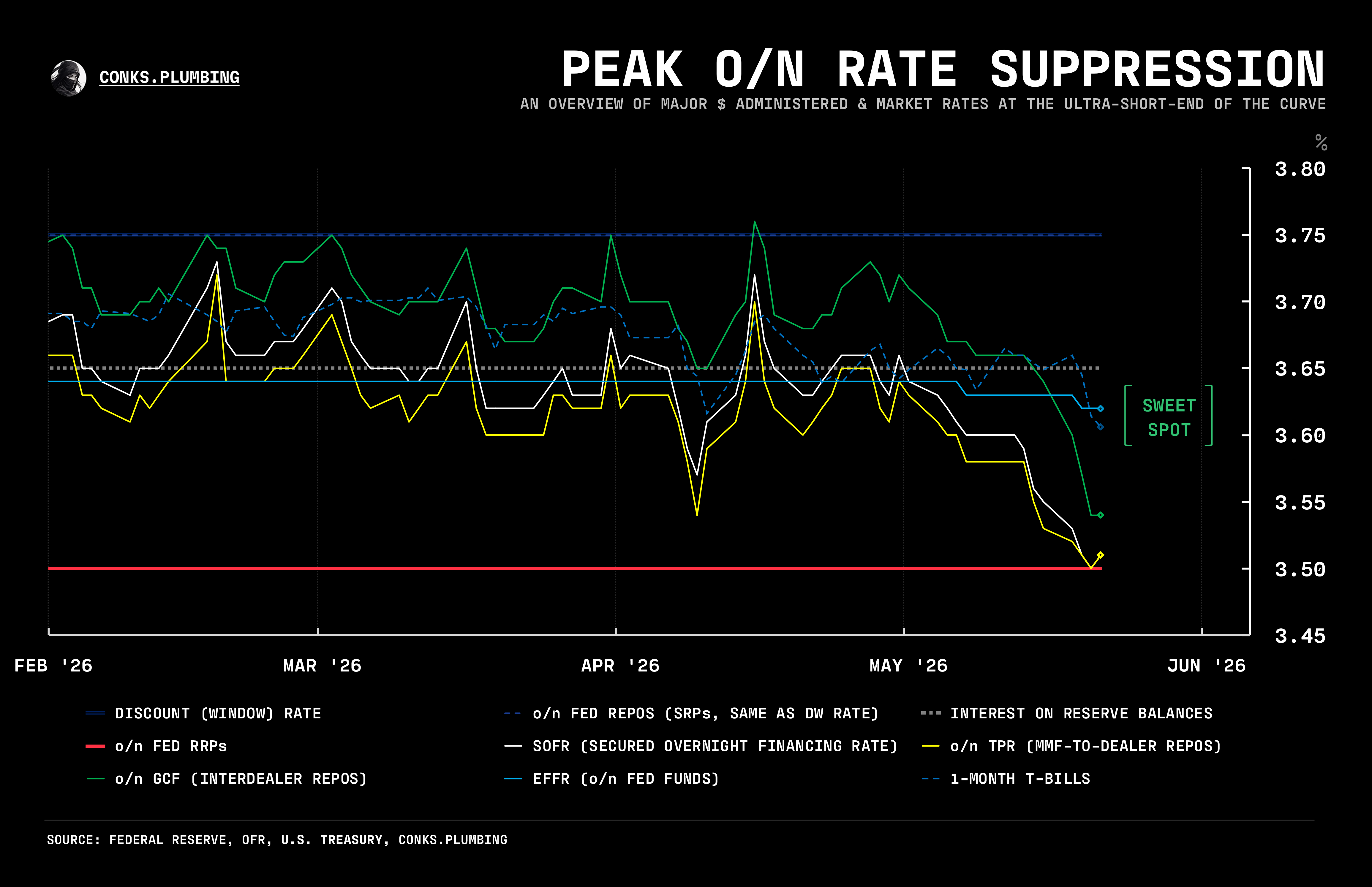

A large imbalance has once again hit the ultra-short-end, this time with too much liquidity driving an epic decline in overnight (o/n) rates. Calling the pre-Warsh period “the calm before the storm” has proven more than an understatement. Just six months ago, the Fed’s alarm system instigated the end of taper1 (i.e. QT) and the start of RMOs2 totaling $40 billion a month. Now the Street is pushing for an imminent halt to Fed reserve injections. The central bank has overshot, with the o/n rate complex3 approaching the lower end of its target range. Officials are thus facing pressure to cease routine interventions. Monetary leaders and trading desks alike, however, must not only navigate this potential “plumbing pause” (in RMOs) but also a subsequent restart. The unwinding of The Fed’s Overshoot is about to commence.

An “unofficial” attempt by monetary leaders to lower money market rates4 has led to an abundance of $ liquidity, a cash flood so powerful that it caused the Fed’s benchmark for interbank rates (EFFR shown above) to finally print lower. Central bank injections combined with numerous catalysts, outside the Fed’s control, have pushed o/n rates to the lower bound. Fed operations have swept up collateral5, the U.S. Treasury has reduced its supply6, and GSE cash has temporarily flooded U.S repo markets. Likewise, “war volatility” has been fueling uncertainty further out on the curve, prompting desks to park more liquidity in money market funds. All these catalysts have generated a cash surge, driving down the ultra-short-end.

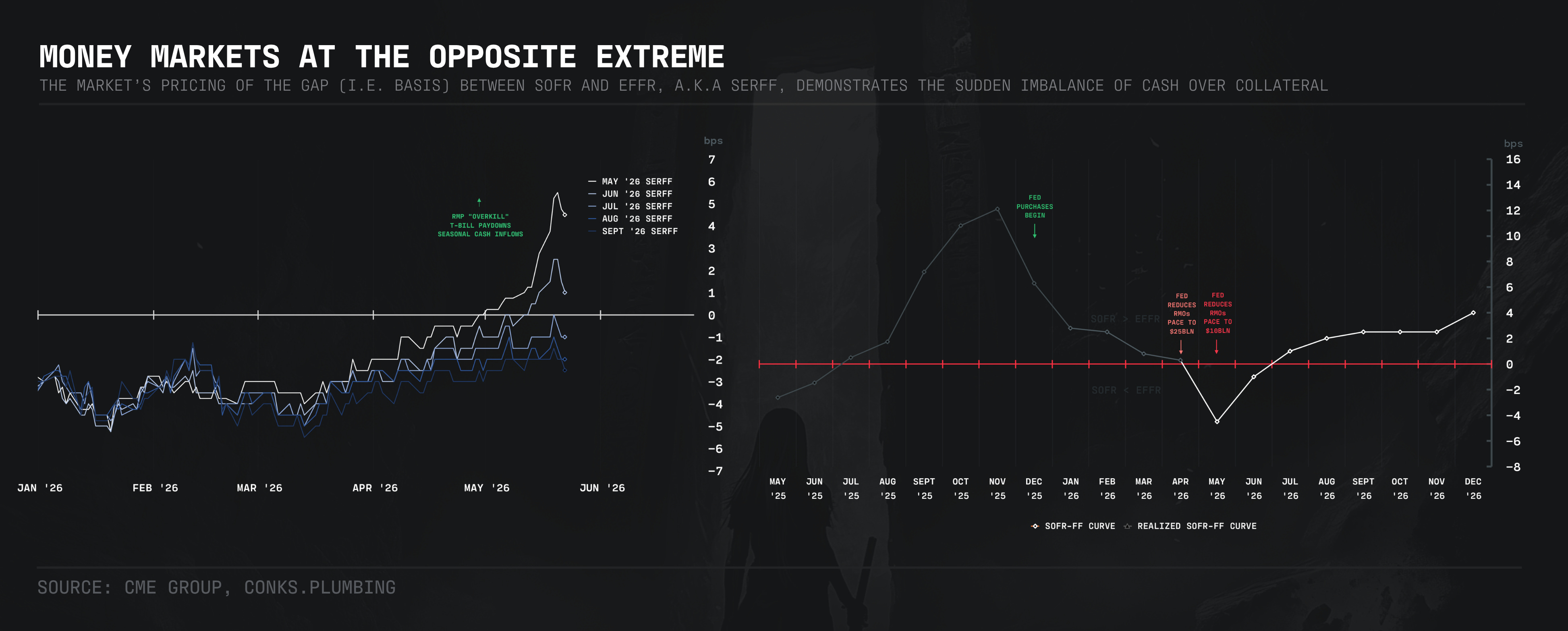

Even so, markets failed to anticipate7 such a sharp plunge in rates8. Its primary driver also remains undetermined. So much so, even the largest dealer desks struggled to decode the puzzle.

What is known, however, is that cash is failing to find adequate paper9. An abundance of cash chasing a scarce supply of collateral has generated an over-compression of money market rates, and its undoing requires creating a drag on $ liquidity. The Fed’s plumbing “reaction function” is thus about to change.