Plumbing Notes: The Warsh Prelude

the calm before a (tepid) money market storm

The Powell era of $ funding markets is set to conclude with volatility approaching all-time lows. The Fed has front-loaded its reserve injections to avoid another repocalypse. Deregulation has boosted swap spreads — Conks’ primary gauge of plumbing conditions, while low volatility from a Great Compression has enabled tighter (i.e. less negative) cross-currency (XCCY) bases. The Warsh era, however, will soon disrupt this status quo. Each proposed shakeup, from reduced Fed guidance to shrinking the central bank balance sheet, shall reintroduce largely unwelcome volatility plus uncertainty into rates and $ funding markets.

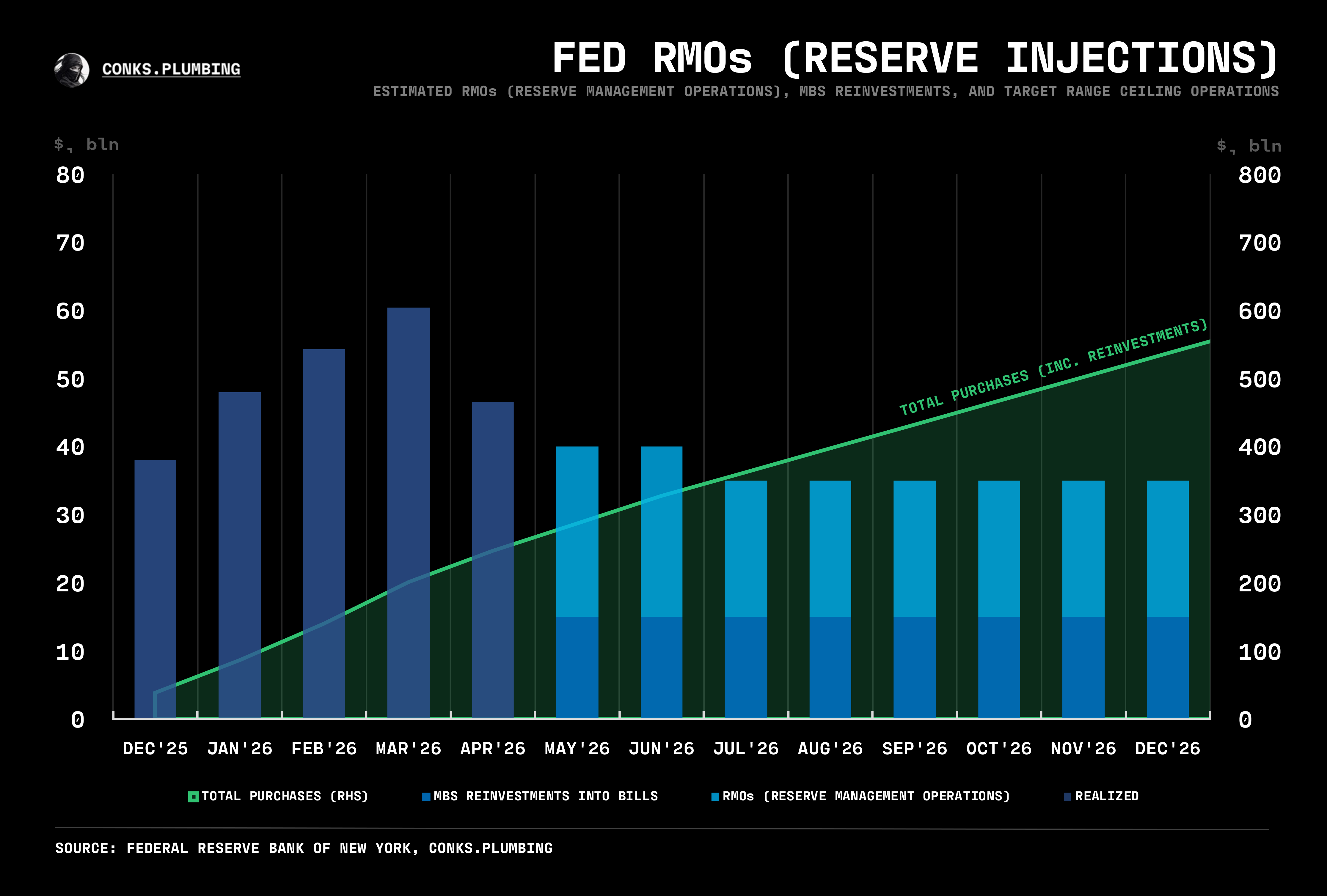

But for at least the next few months, it’s business as usual. The Fed may be reducing its RMOs, yet it’s still pumping $25 billion per month into the interbank ecosystem. The endgame for reserve injections is what Conks calls “reserve stasis”, where the U.S. central bank injects zero net positive interbank liquidity, other than $20 bln in reserves to offset those destroyed1 or neutralized in the TGA or foreign repo pool. A rumored balance sheet shrinkage under Warsh will have to wait, as the Fed’s Old Guard won’t risk tempting fate near the system’s lowest comfortable level of reserves (a.k.a LCLoR).

The Great Compression trade is nonetheless reaching its prime. In Oct’25, traders were betting when the Fed would fire its monetary bazooka. In Dec’25, they moved on to predicting a peak in reserve injections. Now, in May’26, traders are anticipating when the Fed will stop reducing its RMOs, with Powell leaving reserve injections on autopilot2 until a Warsh-led Fed alters the playing field.