The Fed's Global Put: Part I

the U.S. central bank's global dollar backstop and the end of QT

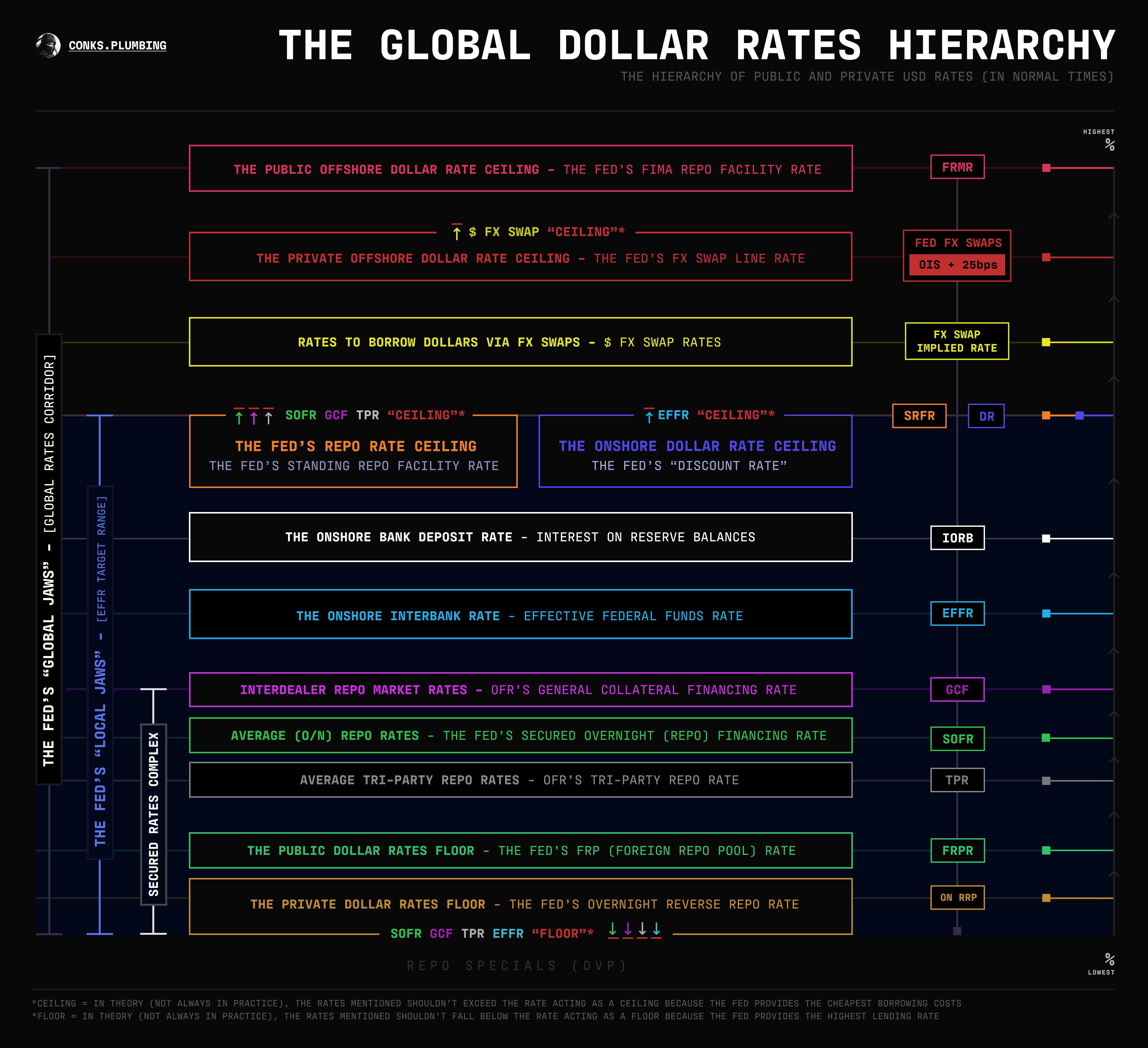

The U.S. central bank is set to strengthen its primary defense mechanism, the Discount Window, deterring systemic bank runs while manufacturing greater demand for reserves and U.S. sovereign debt. This will be one of multiple catalysts forcing dollar market makers to hoard liquidity, decreasing their readiness to step in as private lenders of last resort. Consequently, the Fed’s swap line network — its global defense mechanism — will evolve into a casual source of dollars and less of a backstop, the opposite of what the Fed intends. The U.S. central bank will thus have another motive to end its latest round of QT1 and boost liquidity earlier than expected. Frictions at the top of the dollar rates hierarchy are growing.

Amidst the peak of the subprime meltdown in 2008, a disconnect in the opaquest realm of money markets compelled Fed officials to enforce a truly global dollar backstop. The infamous Lehman Brothers collapse on Sept 15th caused the spread between onshore dollar rates, 3-month OIS2, and offshore dollar rates, 3-month LIBOR3, to widen significantly4. With offshore rates spiking, the fantasy that a global dollar standard was already in effect had been exposed. In response, officials fortified the bridge between offshore and onshore dollar markets by engaging in unprecedented levels of intervention, bailing out the entire money market fund (MMF) complex, cutting rates sharply, and doubling the maximum dollars available to be tapped via swap lines — enacted previously in late 2007 to avert rising turmoil. Nevertheless, the LIBOR-OIS spread kept widening. An enhanced ceiling on global dollar rates was incoming5.

The Fed had two choices to set a tougher ceiling on global dollar rates: enhance its Discount Window or swap line network. The Discount Window allowed foreign banks to pledge collateral at their New York branches, receive emergency dollars from the Fed, extend those dollars to HQ (headquarters), and then lend to frantic offshore borrowers. Swap lines, meanwhile, added foreign central banks into the mix. Acting as brokers, foreign central banks held dollar auctions in their home country, where domestic banks seeking dollars bid for liquidity by pledging sovereign bonds6 as collateral plus a haircut, shielding the central bank from potential losses. The foreign central bank then transferred dollar reserves, credited to its master (reserve) account7 by the Fed, to the foreign banks’ master account. The foreign bank had now acquired access to dollars and could issue dollar loans to customers at its offshore branches. The “cross-border currency repo” (CBCR) was born.

While a global discount window failed to provide dollars to smaller, less connected foreign banks — and their $6 trillion in liabilities, a global swap network could reach every corner of the offshore dollar system and repair the LIBOR-OIS breakage. On October 13th, 2008, the Fed announced unlimited swap lines with every major Western central bank, then the BoJ (Bank of Japan) the following day, bringing the spread back into balance. Limitless “cross-border currency repos” was the fix that would grow to become the new global dollar backstop. Yet, it had not reached its full potency. More than a decade later, a global pandemic would allow monetary leaders to usher in a more powerful weapon.