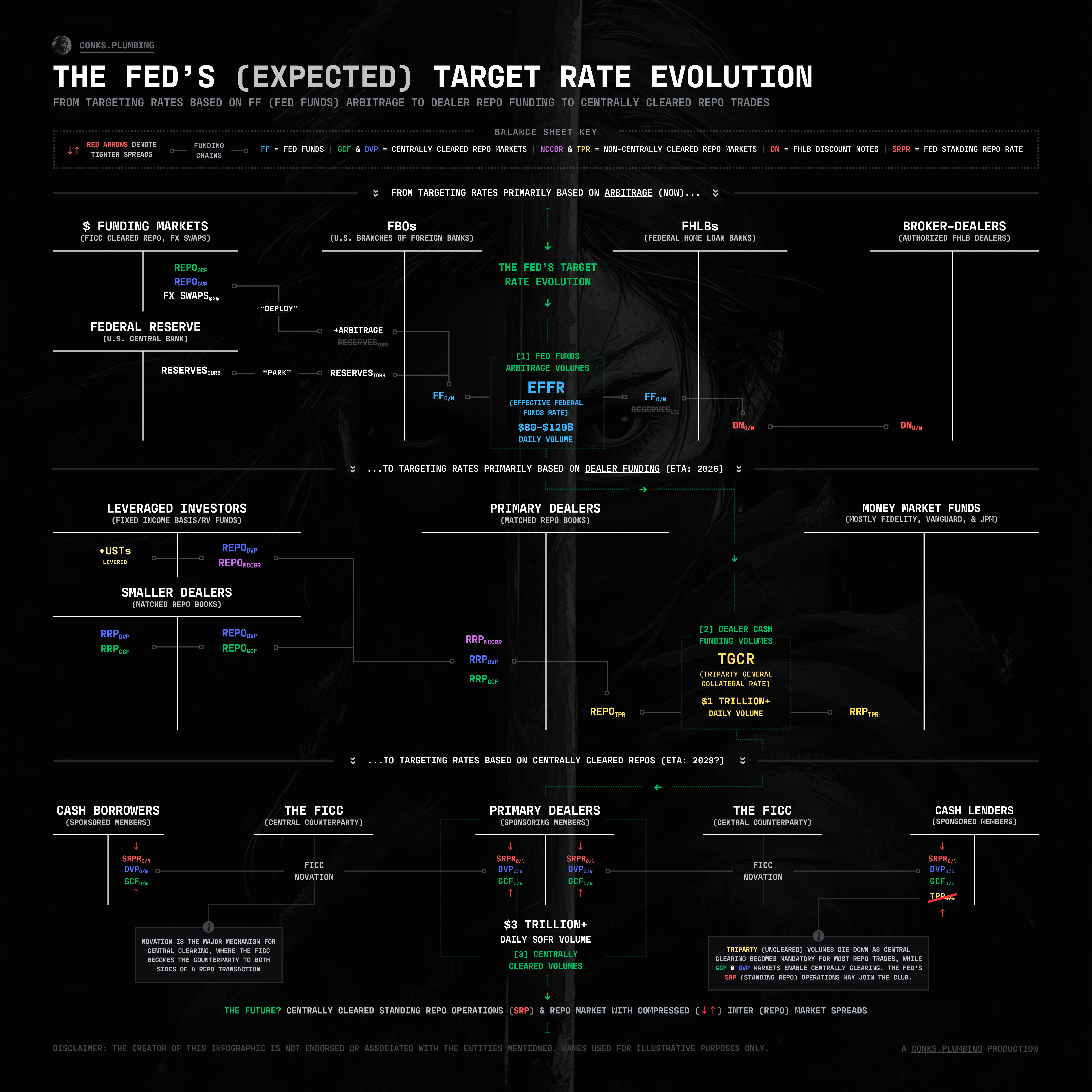

The Fed's New Target: Part II

within the secured rate complex lies a new target rate

— click here for Part I and here for Pro

With a Great Compression in money market rates underway, it’s the ideal moment for Fed officials to switch to a new target rate. As Part I unveiled in detail, volume in overnight Fed Funds (o/n FF) — the average rate of which the Fed currently targets to influence economic and financial conditions — has collapsed. Remaining o/n FF activities also fail to reflect the actual cost of tapping U.S. dollars while remaining vulnerable to a cluster of emerging rival interbank markets. The mechanism underlying the U.S. central bank’s primary monetary tool is thus approaching its breaking point.

For decades, targeting an unsecured interbank rate, such as o/n FF, made total sense. The Fed Funds market thrived and reflected the genuine price at which banks financed their operations. That ended, however, in 2008, with Lehman Brothers’ sudden demise. Unsecured interbank volumes soon fell by ~80%, while reserves injected by the Fed ballooned by multiple trillions. The latter has served as a stabilizing force for EFFR (i.e. o/n FF), enabling officials to avoid updating the target rate for more than a decade. Regardless, instability has risen sufficiently to warrant the next target-rate evolution.

To supplant o/n FF, central bank alchemists will explore multiple configurations: targeting an administered rate (e.g., IORB or o/n RRP), targeting an existing benchmark, assembling a “rates basket” and targeting its average, or constructing and targeting a new benchmark altogether. The ideal successor, though, grows evident quickly.