The Fed's Repo Defensive: Part II

the inner workings of the Fed's emergency repo facility

— click here for The Fed’s Repo Defensive: Part I

The Fed is set to embark on a “Repo Defensive”: the first rework of its Standing Repo Facility (SRF), a mechanism for providing emergency cash loans to banks and primary dealers. Another cash squeeze at the end of September revealed key market makers’ reluctance to use the SRF, a sign that the Fed’s facility may fail to stem money market contagion. Yet, even with upcoming fortifications, the repo market will remain the most systemic yet fragmented part of the dollar system. Consequently, Fed architects must remove barriers deterring dealers from tapping the SRF before the next storm emerges. The first iteration of the Fed’s repo “defense mechanism” is approaching.

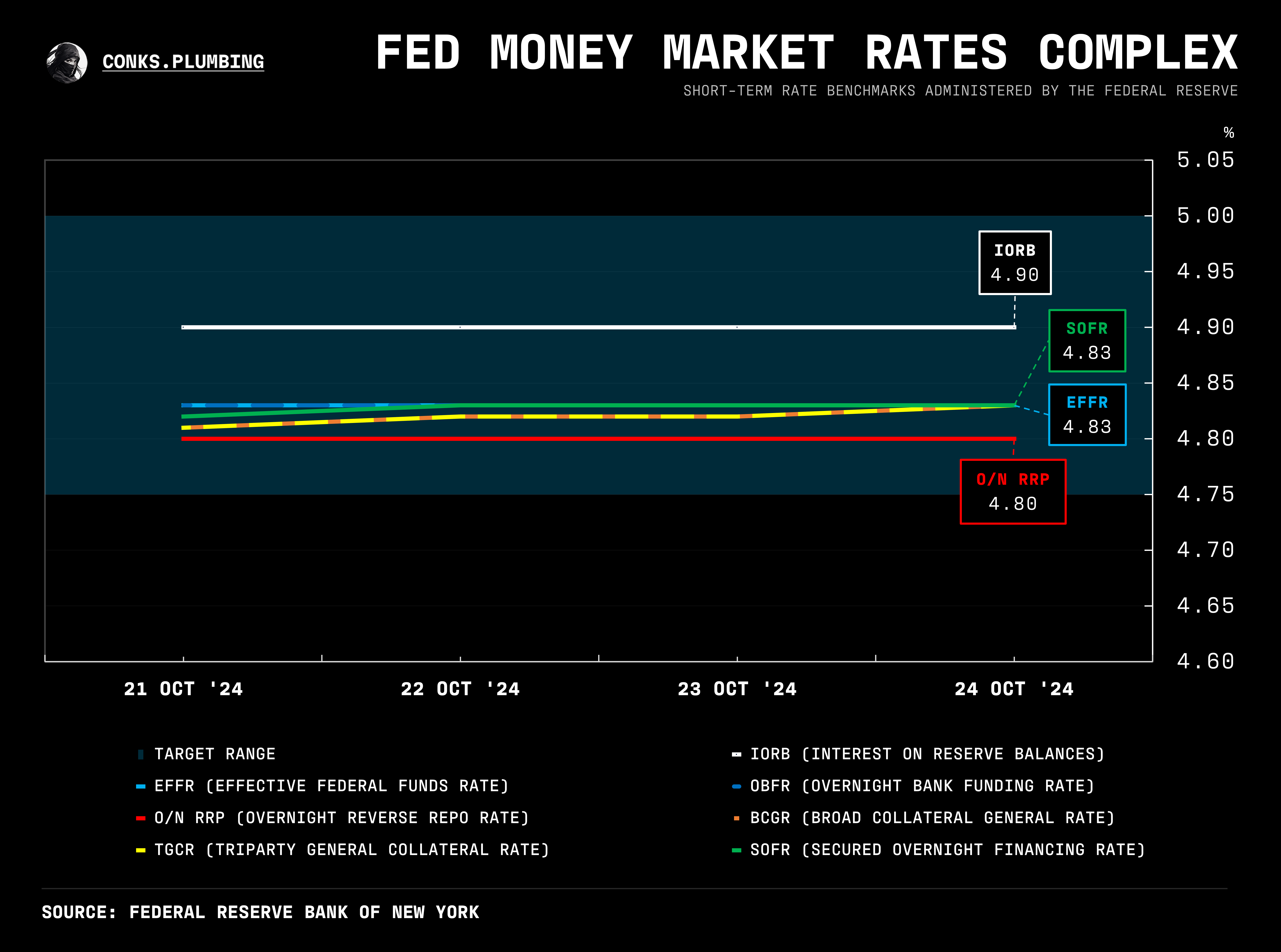

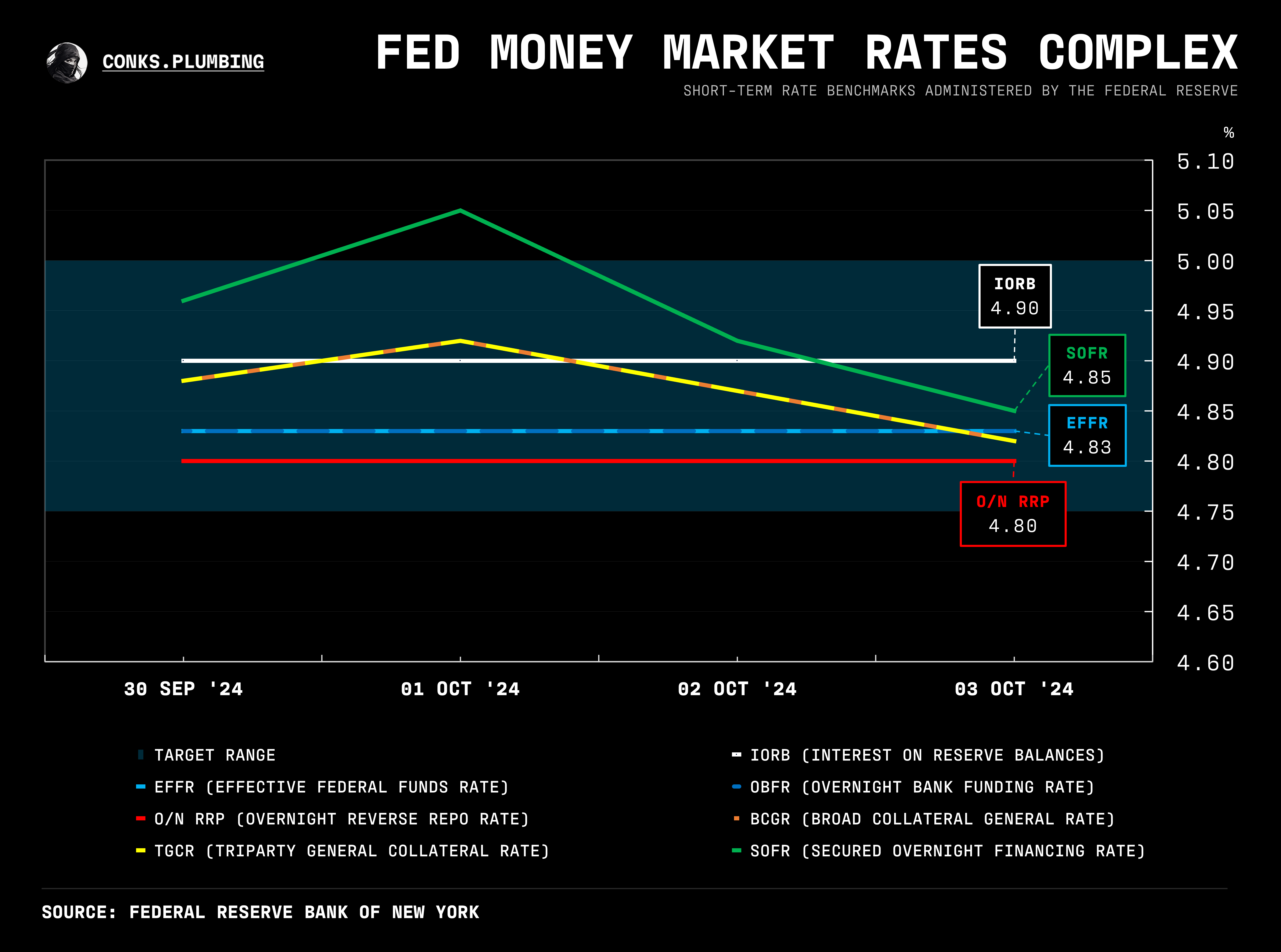

During the latest September quarter-end1, another liquidity squeeze arose. Dealers, as usual, were pulling back from market-making to tidy their balance sheets. Meanwhile, money funds (MMFs) reached their self-imposed counterparty lending limits, parking their leftover cash in the Fed’s RRP while rejecting bids from major market makers. By lunchtime, dealers glanced at their screens and witnessed repo rates blowing through the top of the Fed’s target range. A mild cash shortage had developed. At 1:30pm, primary dealers were forced to tap the Fed’s repo facility, with the U.S. central bank again becoming a dealer of last resort, bridging all market imbalances.

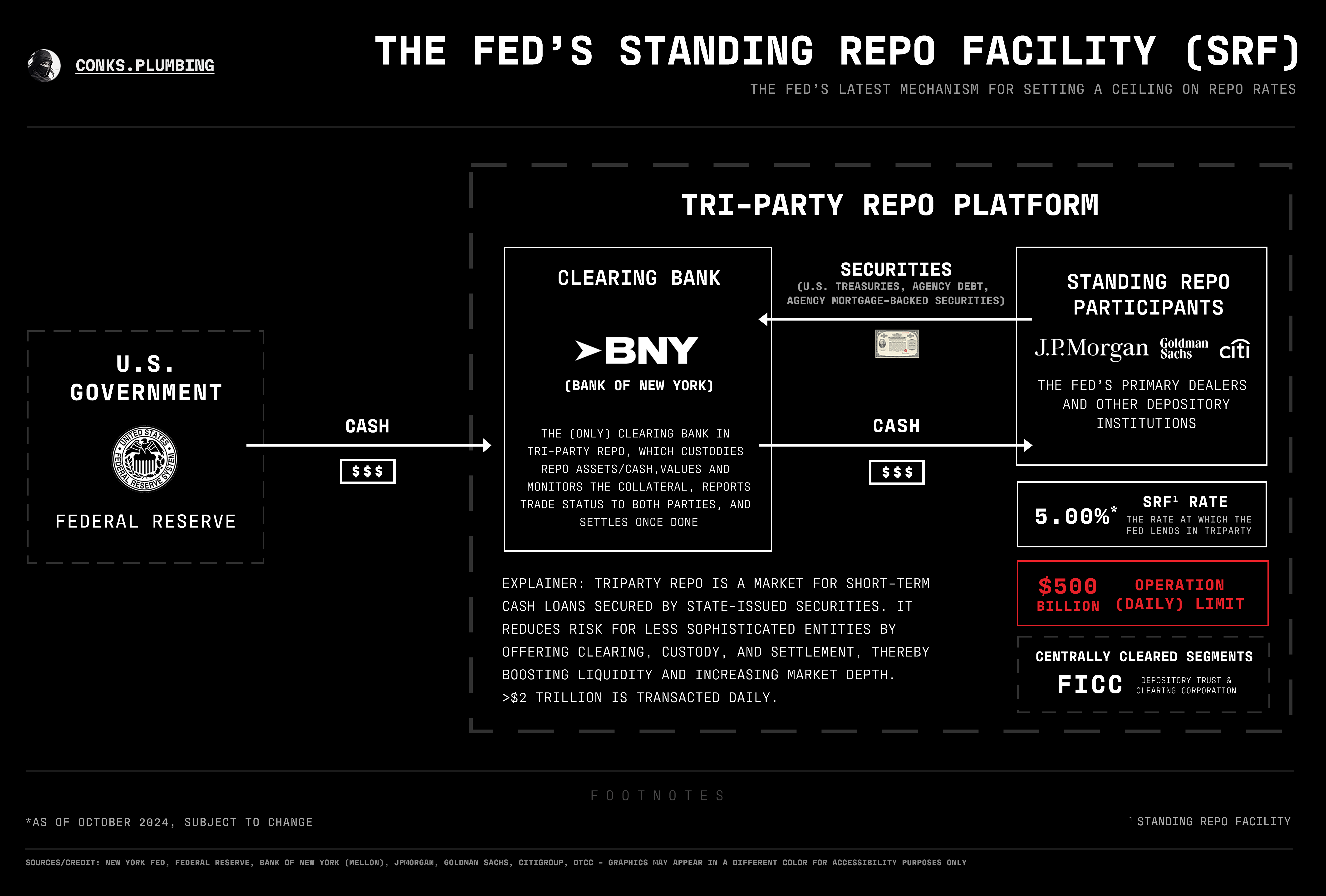

That day, over $600 billion in repos traded above “SRFR”2: the cheapest rate offered on overnight (o/n) Fed repos — i.e. cash loans from the U.S. central bank secured against sovereign bond collateral. Rather than tapping the $500 billion available at the facility, dealers borrowed a mere $2.6 billion, suggesting market makers failed to take advantage of cheaper cash lending rates. But in complex markets, things aren’t always what they seem. It appeared dealers could earn a juicier spread by lending cash from their clearing accounts3 in the morning, waiting until 1:30pm (when the SRF opens), and covering the amount via the Fed rather than in costly private markets. In reality, however, timings dictate dealers’ actions. During morning trading, market makers provide most liquidity between 7-9am to maintain key client relationships and avoid negative balances (i.e. overdrafts) in their trading accounts — which incur fees levied by their clearing banks4 at 8:30am. What’s more, repo rates remain volatile intraday. Lending in the morning in anticipation of borrowing from the Fed in the afternoon creates interest rate risk for repo desks operating “matched books”5. Market makers will thus execute their trading activities as soon as possible, many hours before the SRF opens.

Subsequently, as intended, the Fed’s o/n repo facility serves as a dealer of last resort, not a “hard ceiling” that holds repo rates within central bank targets. Almost every month-end and quarter-end, SOFR — the Fed’s repo rate benchmark — exceeds the U.S. central bank’s target range while officials barely react. Instead, they hope the SRF’s significant defects will only be revealed when the next money market crisis arises and fails to provoke mayhem. Recent episodes, meanwhile, show the SRF needs to evolve so that market makers access emergency repos without friction, preventing spillovers6 into other markets that prompt a (reluctant) Fed to end QT early. The U.S. central bank must now introduce more alluring features.

{kind=link}

{kind=link}

Coincidentally, in both macro and plumbing realms, a previously reactive Fed is becoming proactive. An SRF rewire will shortly hit their agenda. Even so, revamping an o/n repo facility is far from straightforward. To illustrate the elaborate task Fed architects face, we must turn to the SRF’s inner workings.