The Money Market Blindspot: Part II

volatile flows could impede the Fed's "alarm system"

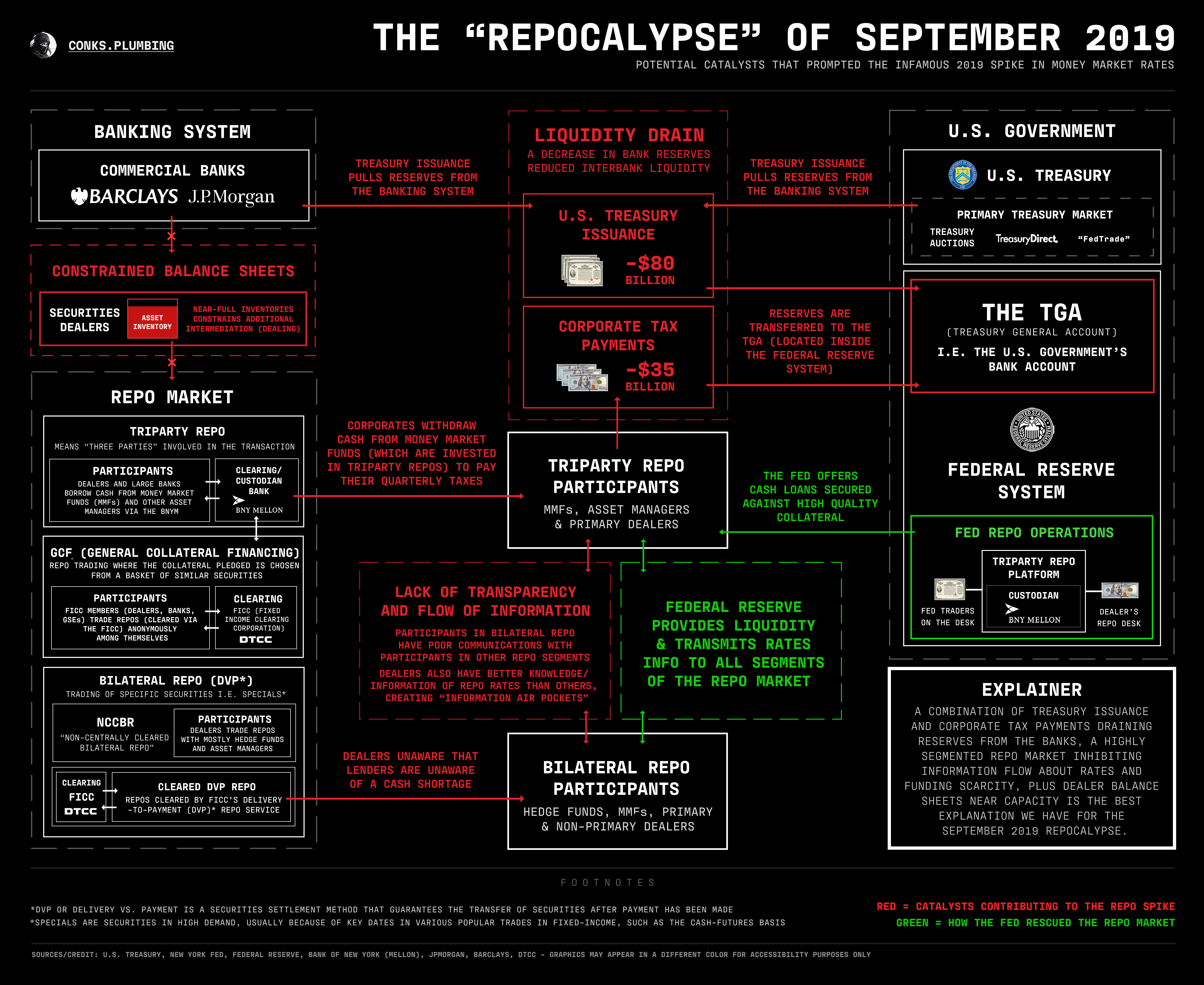

— click here for The Money Market Blindspot: Part I

Another debt ceiling battle is set to induce volatility in money markets. Under the command of newly sworn-in Scott Bessent, the U.S. Treasury has started employing “extraordinary measures” to bypass a now-binding debt limit1. Yet, these gimmicks won’t last forever. Soon, America’s checking account, the TGA2, will be drawn down, releasing a flood of liquidity into the banking system. Anticipating a cash surge in the first half of the year, the SOFR-FF (SOFR-Fed Funds) futures curve3 — a measure of expected funding conditions — has thus priced in a looser environment4. This easier climate, however, will soon be altered by a giant collection of tax receipts5, an unwind of liquidity that could be deepened by a parallel debt limit resolution6. With not only the U.S. government’s bank account but the RRP also complicating flows, the Fed’s liquidity “alarm system”, eager to front-run7 the next money market upheaval, is about to face its first major hurdle.

{kind=link}

At the latest FOMC meeting, monetary leaders again confirmed their desire to maintain the smallest possible balance sheet8, superseding their urge to end QT9 and thwart another money market seizure. Consequently, only an unforeseen rate spike will compel officials to abandon their objectives. But for now, reserves lost to the U.S. central bank’s “QT shredder” will be more than offset by Sec. Bessent drawing down (i.e. draining) the TGA10, lowering repo rates — while costs to borrow overnight Fed Funds (o/n FF) continue to flatline. The U.S. central bank’s premier gauge of reserve scarcity, RDE (Reserve Demand Elasticity)11, hovers around zero, implying subtle changes in reserves will fail to drive o/n FF toward the top of the target range and disrupt the Fed’s goals. Without RDE falling sharply negative12, the Fed will have the conviction to continue its balance sheet “runoff”13, an action the U.S. central bank no longer deems tightening but a “normalization”. Volatility in funding markets is subsequently looming.

Unfortunately for officials, upon a debt limit resolution, a TGA drawdown will evolve into a TGA refill14, where both dollar funding and liquidity tighten. Short-term desks and STIR traders15 appear to be pricing an end to easing sometime in Q2, as the SOFR-FF futures curve turns from flat and positive to downward and negative16. A double whammy of tax receipts and a TGA cash reload is about to produce turbulent money market flows, but with volatility comes opportunity.