There was some confusion as to what the SOFR-FF basis & SOFR-FF basis spreads mean (and imply), which is no surprise, given it’s one of the most niche instruments out there.

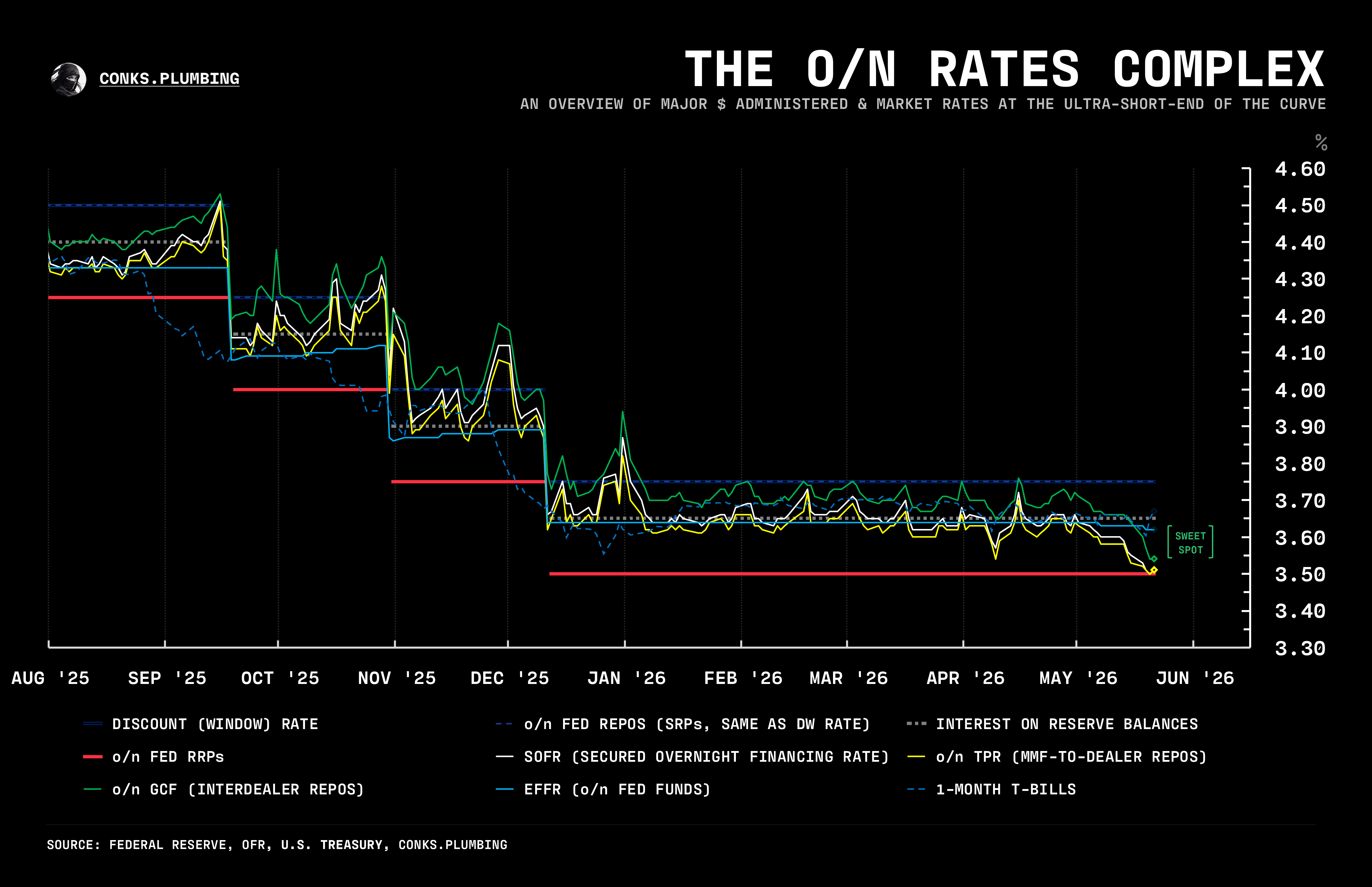

First, it’s useful to distinguish between “SOFR-FF” and “SOFR-FF basis”. These terms have the same meaning: simply, the Fed’s SOFR (repo rate benchmark) minus the Fed’s EFFR (average overnight unsecured lending rate between banks) — where “FF” (Fed Funds a.k.a bank reserves) is used as a shorthand for EFFR.

If SOFR “prints” (i.e. is published) at 4.00% and FF at 3.90%, SOFR-FF (i.e. a shorthand for “SOFR-FF basis”) equals 10bps (4-3.90=0.10=10bps), and thus a measure of liquidity conditions that most would consider tight: a wider (i.e. more positive) SOFR-FF basis usually implies tighter funding conditions, and vice versa. SOFR is an active market, so rates move with liquidity conditions, while the Fed Funds market remains “undead”, with only ~$100bln in volume. EFFR tends to print in a straight line unless we see a large cash influx or outflow at the ultra-short-end.

You can view the “front-month” SOFR-FF basis (i.e. June 2026) via TradingView by searching: CME:SR1M2026-CBOT:ZQM2026 - but before you view this, please read on...

To take it a step further, a SOFR-FF basis SPREAD is the difference between two SOFR-FF bases (plural of basis) at two different times. This shows the relative (expected) liquidity/funding conditions between two periods. For instance, July 2026 and Sept 2026 may have differing catalysts, like varying bill issuance and demand for leverage, etc., that produce different “implied” (i.e what the futures market thinks of) conditions and therefore different expected SOFR-FF bases.

You can view the basis SPREAD between July ‘26 & Sept ‘26 via TradingView by searching: CME:SR1N2026-CBOT:ZQN2026-(CME:SR1U2026-CBOT:ZQU2026) or on BBG via SERFFN6/U6 (note: CBOT is part of CME). The letters “N” and “U” represent July & September, not the first characters of months. Instead, CME uses the following letters (known officially as “calendar codes”):

January=FJuly=N

February=G

March=H

April=J

May=K

June=MAugust=QSeptember=U

October=V

November=X

December=Z

Now, let’s say the market thinks (note: not a real-world situation and using round numbers, instead of real-time quotes, for clarity) the gap (i.e. basis) between SOFR and FF in July 2026 will be 10bps wider than that in September 2026, due to reserve injections by the Fed happening in September but not in July, resulting in a larger gap between SOFR and FF in July 2026 than in September 2026. The math laid out may assist in understanding:

July 2026 SOFR-FF basis = 4.10-3.90 = 20bps

September 2026 SOFR-FF basis = 4.00-3.90 = 10bps

Jul/Sept’26 SOFR-FF basis spread = (July) 20bps - (Sept) 10bps = 10bps

However, you will likely be viewing the spread via futures, where contracts are priced at 100 minus the implied market rate. Subsequently, a positive SOFR-FF basis will be priced as a negative value, and vice versa, in the futures market. “Quick maths” shows this in action:

realized (i.e. the Fed’s published data for SOFR and EFFR):

4.00 - 3.90 = 0.10 = 10bps

...but in futures pricing:

(100-4.00)-(100-3.90) = -0.10 = -10bps

So when the futures market for SOFR-FF basis “sells off”, that’s the basis getting larger (suggesting tighter funding conditions), not narrowing. Again, some quick maths:

before: (100-4.00)-(100-3.90) = -0.10 = -10bps

after: (100-4.00)-(100-3.85) = -0.15 = -15bps

Accordingly, a -0.15 (-15bps) futures spread actually means an average SOFR-FF of +15bps for a certain month, and an increase in the SOFR-FF basis of +5bps in the above example.

Using another example, let’s say the SOFR-FF futures basis is priced at -10bps on the last day of July 2026, and let’s say it never changes until the end of July. SOFR stays at 4.00, and EFFR stays at 3.90. Subsequently, the “realized” SOFR-FF basis (i.e. using the Fed’s published data for SOFR and EFFR) equals 10bps (0.10), but the SOFR-FF basis in the futures market will be priced at -10bps (-0.10).

The same applies to SOFR-FF basis SPREADS. To simplify, participants tend to use jargon: “July/Sept‘26 SOFR-FF” is used to denote the SOFR-FF basis SPREAD between July 2026 and Sept 2026 i.e. the difference in the SOFR-FF basis between Jul’26 and Sept’26. The jargon for the futures market is “Jul/Sept‘26 SERFF”, where SERFF is just the futures market ticker for the SOFR-FF basis on Bloomberg terminals. Some SOFR-FF traders will call themselves “SERFF traders”.

Hence…

Jul’26 SERFF in futures market = (100-4)-(100-3.80) = -0.20

Sept’26 SERFF in futures market = (100-4)-(100-3.90) = -0.10

futures basis spread (Jul/Sept‘26 SERFF): -10bps

actual SOFR-FF spread (Jul/Sept‘26 SOFR-FF) priced at: 10bps

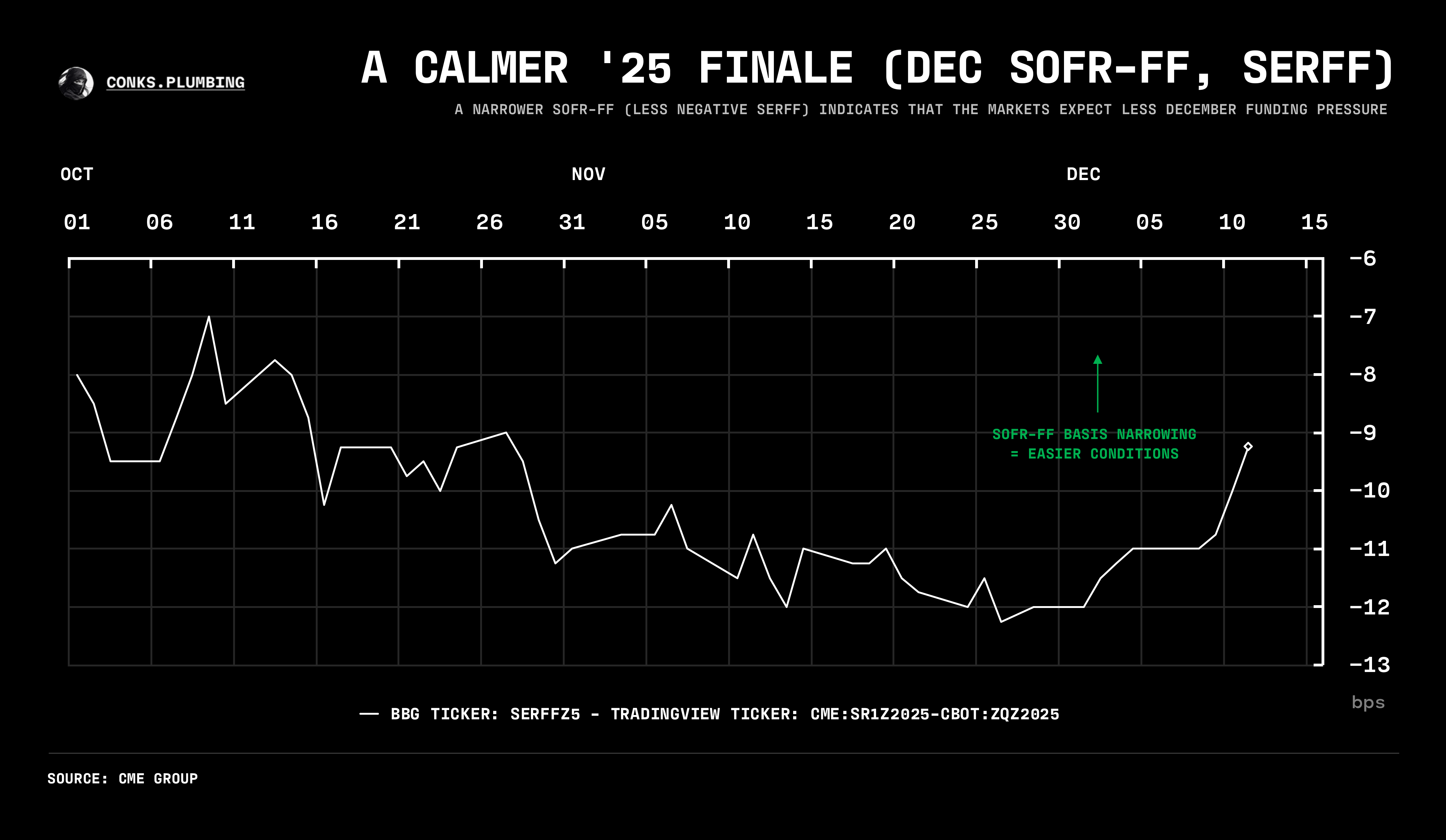

In English, we have a 10bps wider SOFR-FF basis priced in for July than September because the futures market calculates everything “upside down”. Since a wider1 basis (in our simplified world) implies tighter conditions, the market expects tighter funding conditions in July than in September. This will be reflected in the futures market for SOFR-FF “selling off”. For instance, in December 2025 (last year), Dec’25 SERFF sold off as the Fed’s QT was set to tighten conditions, until rumors of QT ending arose.

Why bother learning this? The SOFR-FF basis is considered the primary proxy for liquidity conditions (and with basis spreads, relative conditions) in money markets, and something you should add to your arsenal. Every rates desk will trade this and have a house view on SERFF, the most common lingo for SOFR-FF. Although some city traders and dealers prefer a variety of phrases.

That’s a wrap. Follow snapshots for daily SERFF!

confusing tidbit: so even though the SOFR-FF basis is widening (getting larger), the convention used by some analysts is to say they expect SOFR-FF to tighten (and vice versa), so it’s good to double-check with the analyst!